In the past, we’ve posted all the studies, data, and other information we’d compiled in support of the 199A deduction (here and here).

With Congress debating the deduction once more – Ways and Means hearing tomorrow! – we thought this would be a good time to repost all this work. It demonstrates both the importance of the pass-through sector to the economy and the importance of Section 199A to the pass-through sector.

The Importance of 199A

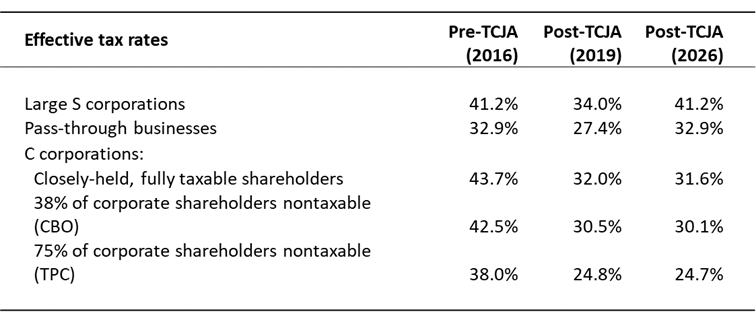

Our recent study by EY’s Robert Carroll demonstrates how the 199A deduction is vital to Main Street parity. The key takeaway is summed up in the table below – the TCJA established rough parity between public corporations and pass-through businesses, but only as long as section 199A is in place. Without 199A, pass-throughs lose out to large, public corporations regardless of what assumptions you make about their size or shareholder makeup:

EY’s numbers aren’t an aberration. Numerous economic studies from the CBO, Treasury, and the private sector all come to a similar conclusion – the effective marginal rates faced by corporations and pass-through businesses post-TCJA are roughly equivalent, but only with section 199A in place. Without section 199A, the comparative rates aren’t even close:

| With 199A Deduction | Without 199A Deduction | |||

| C Corporation | Pass-Through | C Corporation | Pass-Through | |

| DeBacker & Kasher — Market Returns (AEI) | 19.0% | 20.0% | 19.0% | 27.0% |

| DeBacker & Kasher — Above Market Returns (AEI) | 16.0% | 21.0% | 16.0% | 30.0% |

| Barro & Furman (Brookings) | 26.0% | 31.1% | 26.0% | 35.5% |

| Treasury (2021) | 18.9% | 24.2% | 23.2% | 26.4% |

| EY (2023) | 24.8% | 27.4% | 24.7% | 32.9% |

| CBO (2024) | 17.0% | 21.0% | ||

Resources:

- Ken Kies (Op-Ed, Tax Notes): The Ryder Cup and Section 199A – Really!

- EY Study: Relative Tax Treatment of Pass-throughs and C Corporations

- S-Corp: The Importance of 199A

- S-Corp: The Main Street Defense of the 199A Deduction

- S-Corp: Nichols Explains 199A in Tax Notes

- Joint Trades Letter on 199A Permanence

Section 199A Sunset Puts Millions of Jobs at Risk

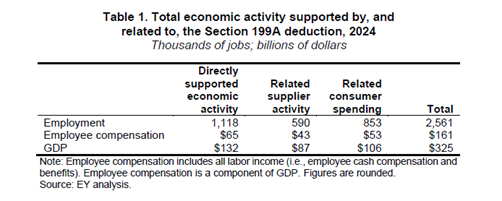

Section 199A supports millions of jobs – jobs that will be put at risk if Congress allows the deduction to sunset. That’s the key take-away from last year’s EY study on the economic footprint of Section 199A.

What did EY find? Section 199A supports 2.6 million jobs, contributes $161 billion to employee compensation, and adds $325 billion to the national economy:

These results highlight the importance of Section 199A and how the expiration of the deduction threatens these jobs. Absent congressional action, 2.6 million jobs will be at risk.

Bottom Line:

- The Section 199A small and family business deduction supports 2.6 million jobs in the United States.

- Allowing 199A to sunset puts all those jobs at risk, resulting in less employment, lower wages, and a smaller economy.

- Congress needs to protect Main Street and the people who work there by adopting the Main Street Certainty Act and make permanent the 199A deduction.

Resources:

- EY Study: Economic activity supported by the Section 199A deduction

- S-Corp: 199A EY Study Briefing Recap & Recording

- Congressman Smucker Press Release

Public Corporations and the Double Tax

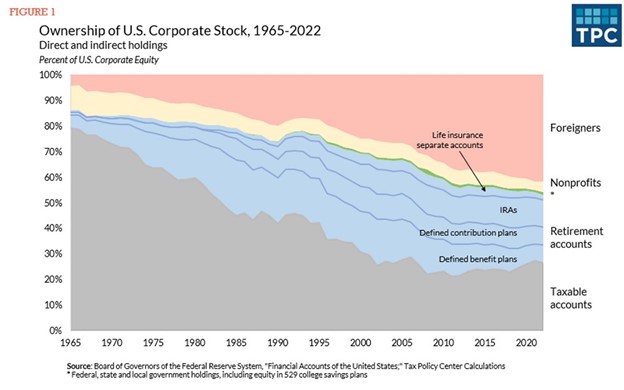

On paper, C corporations face steep tax rates due to the so-called double tax. This theoretical double tax has fooled many observers into believing that public corporations face effective tax rates approaching 40 percent.

The reality, however, is that most corporate shareholders pay little to no tax, largely eliminating the second layer of tax. The Tax Policy Center has the latest data on this front, finding the percentage of taxable shareholders has declined from around four in five back in 1965 to only one in four today:

This means the effective tax rates paid by public corporations are significantly lower than the advertised rates (see the first section for the estimates). They also are far below what comparably-sized pass-throughs face. In an excellent defense of the 199A deduction, former JCT head Ken Kies addressed this issues back in 2021:

…In the United States it’s common to talk about the double tax on corporate earnings. As a general proposition, it’s not fake news: A corporation pays tax on its earnings and the owners of corporations — that is, the shareholders — generally also pay tax on any remaining earnings that are distributed to them.

Based on the best available data, it’s estimated that no more than 9 percent of annual corporate profits are subject to tax a second time, and no more than 14 percent will eventually be taxed upon later distribution (that is, as taxable pension or retirement account distributions). That means that only around a maximum of 23 percent of U.S. corporate earnings ever face a second layer of taxation.

So-called experts who ignore the reality of who owns public corporations today are doing a disservice to the public debate.

Resources:

- Tax Policy Center: Grappling with a Dwindling Shareholder Tax Base

- S-Corp: The “Experts” Get 199A Wrong, Part 2

- S-Corp: S-Corp: C Corps for Everybody?

Employment Numbers Confirm Pass-Through Importance

Individually- and family-owned businesses comprise the vast majority of businesses, they employ the majority of private sector workers, and they do so literally everywhere. They are the foundation upon which thousands of communities across this country are constructed.

Analysis shows just how many Americans are employed by individually- and family-owned businesses in each of the country’s 435 Congressional districts. The results are impressive and reveal just how important private businesses are to this nation. Below are a few highlights:

- Pass-through businesses, including S corporations, partnerships, and sole proprietorships, employ 62 percent of the American workforce;

- Private companies (pass-through businesses plus private C corporations) employ 80 percent of workers;

- For every worker employed by a public C corporation (27 million), there are more than four employed by a private business (113 million); and

- Of the 435 total Congressional districts in America, private companies are responsible for 80 percent or more of total employment in 316 of them.

Why does this matter? Because the expiration of the individual and pass-through tax provisions next year would disproportionately harm private businesses, putting those jobs at risk.

The Main Street Tax Certainty Act introduced by Representative Lloyd Smucker and Senator Steve Daines would make 199A a permanent fixture of the code, staving off a massive tax hike and providing these businesses with much needed certainty. It is supported by over 160 national trade associations and is cosponsored by more than 190 Congressmen and more than 30 Senators.

Resources:

- S-Corp: Mobile App

- EY Study: Employment Data by Congressional District

- EY Study: Full Dataset

- Smucker 199A Permanence Bill (H.R. 4721)

- Daines 199A Permanence Bill (S. 1706)

- Joint Trades 199A Support Letter

199A Essential for Economic Growth

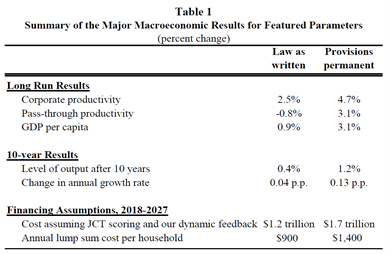

Pass-through businesses employ the majority of private sector workers (62 percent) so any increase in their taxes would have broad negative effects on the economy. A Brookings paper authored by Robert Barro and Jason Furman isolates the economic impact of the sunsetting TCJA provisions, including the 199A deduction, the lower individual rates, and expensing:

As you can see, the ‘law as written” column shows pass-through sector productivity under the TCJA is negative. This result is due to the sunsets starting in 2026, plus the TCJA’s base broadening provisions that remain in place. These provisions include the cap on interest deductions, forced amortization of R&E expenses, and the many other business tax base broadening provisions in the TCJA.

The result would be a significant tax hike on pass-through businesses – not relative to tax policy in 2024, but relative to tax policy pre-TCJA. After all the talk of supporting Main Street, going off the fiscal cliff next year means the Trump “tax cuts” would raise taxes on millions of Main Street businesses, just to cut them for Apple and Amazon.

Resources

- Main Street Employers Coalition: Section 199A One-Pager

- Brookings Institute (Robert Barro, Jason Furman): The Macroeconomic Effects of the 2017 Tax Reform

- S-Corp Advisor Lynn Mucenski-Keck: Small Business Committee Testimony

- S-Corp: Pass-Through Businesses & Tax Policy

- S-Corp: More on the Wyden 199A Bill

- S-Corp: A Modest Tax Hike? Not Even Close

- S-Corp: Tax Hike Premise Takes Another Hit

199A Offsets

One objection to Section 199A permanence is it would lose revenue at a time when deficits are large. This concern ignores the fact that the 199A deduction wasn’t adopted in a vacuum. In fact, it was paired with numerous offsetting provisions that raise lots of money – more than 199A costs, actually – and they primarily target upper-income business owners. These provisions include:

- SALT Cap

- Section 461(l) Excess Loss Limitation Rules

- Section 174 R&E Amortization

- Section 199 Manufacturing Deduction Repeal

- Section 163(j) Interest Deduction Cap

- Section 212 Deduction Limitations

As noted above, many of these provisions are permanent and will stay in the tax code even as 199A expires, resulting in a significant tax hike on pass-through businesses. That hike is not relative to the TCJA, but rather the tax code that preceded it.

When Congress addresses the fiscal cliff this year, we fully expect these revenue offsets to be part of the discussion, so for those policymakers worried about adding to the deficit, be assured that we have you covered.

Resources:

- S-Corp: The “Experts” Get 199A Wrong

- S-Corp: A Rate Hike by Any Other Name…Would Still Kill Family Businesses

- S-Corp: White House Shortchanges Main Street

- S-Corp: An Anti-Main Street Budget

- S-Corp: New Budget Continues the Assault on Main Street

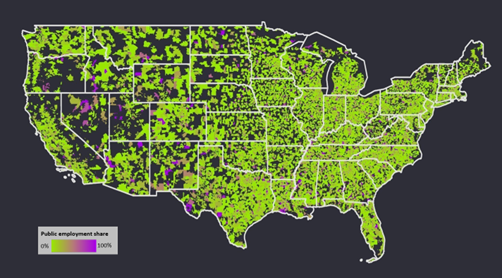

Where the Jobs Are

The fight over section 199A has geographical implications too. In a 2021 Wall Street Journal op-ed, S-Corp President Brian Reardon wrote:

A new study from EY demonstrates that private companies supply the vast majority of business-sector jobs nationally—77% of them. Public companies supply only 23%. As important, private-company employment is spread evenly across the country while public-company jobs tend to be concentrated in a few cities and states.

The op-ed references a study showing just how important private companies, including small and family-owned businesses, are to the large swaths of the United States. While public company employment is concentrated on the coasts and city centers, private business employment is spread more evenly across the country, including 22 states where private companies account for more than four out of five workers.

For members of Congress representing those states and districts, pay attention. Getting the balance right between private and public companies is critical to the economic future of your community.

Resources

- Op-Ed, WSJ: The Democratic Plan to Soak Main Street

- S-Corp: Where the Jobs Are

- EY Study: Distribution of Private and Public Company Employment Across the United States

Voter Support

The Gazette featured an op-ed on how Americans really feel about raising taxes on individually- and family-owned businesses and farms:

Contrary to what the White House might tell you, a new poll conducted on behalf of the S Corporation Association confirms that American voters do not support aggressive tax policies or those that target individually- and family-owned businesses and farms.

The results of the survey referenced above were later presented on a webinar by David Winston of the Winston Group, but they speak clearly to the debate before us as well. American voters do not support taxing Main Street.

One reason voters oppose raising taxes on Main Street businesses is they see these tax hikes as inflationary:

Over half the country (52%) believes a tax increase would increase inflation, rather than decrease (11%) or have no impact (19%). Among independents, 55% believe it will increase inflation (7% decrease, 17% no impact).

Keep in mind these findings are from late 2021, well before inflation spiraled out of control.

Resources

- Op-Ed, The Gazette: Biden’s Tax Hikes are Unpopular and Congress Knows It

- S-Corp Webinar: What do Voters Really Think About the Biden Tax Plan?

- Survey Findings

Conclusion

The 2025 fiscal cliff presents an existential crisis for private companies and the workers and communities that rely on them. Absent action, the expiration of the TCJA’s pass-through provisions would accelerate the consolidation of economic power and decision making into the C-suites of a few thousand public companies, leaving thousands of communities worse off.

For anyone still on the fence, we urge you to read the materials outlined above. For those who already understand how critical this fight is, it’s time to engage. Individual and family-owned businesses are the bedrock of local communities nationwide and they work hard to improve the lives of their employees and neighbors every day. That message won’t be heard, however, if family businesses stay on the sideline.