Horizontal Equity and Section 199A

Thanks to the OB3, Section 199A is now a permanent fixture of the Tax Code. Millions of small and family-owned businesses can now stop worrying about their taxes and refocus on growing and hiring. It’s a good thing that means more investment and jobs on Main Street.

That doesn’t mean the debate is over, however.

A Congressional Research Service (CRS) report, for example, included a nice overview of the provision, but also made a point about horizontal equity we’ve seen previously:

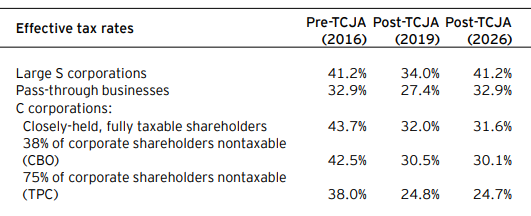

The deduction may diminish horizontal tax equity in two ways. First, it taxes wage earners and pass-through business owners with similar income at different rates, even though there is no apparent economic justification for such disparate treatment.

To illustrate this point, assume that a sole proprietor and an employee have the same taxable income ($100,000 in 2024), and that the former’s income comes solely from QBI for a retail business she owns and the latter’s income is from wages only. Both are single filers. Under the federal individual income tax rate schedules for 2024, the sole proprietor is eligible for the maximum Section 199A deduction, which reduces her top marginal tax rate from 22% to 17.6% (22% x 0.8). By contrast, because the employee cannot claim the deduction, her income is taxed at 22.0%. Under pre-TCJA tax law, both taxpayers would have been taxed at the same top marginal rate.

In other words, two similarly situated taxpayers (horizontal, if you will) are treated differently because of Section 199A. But are they really similar? Is the wage earner really at a disadvantage? Finally, is this the correct comparison?

The answer to all these questions is an emphatic “No”. Treating wage earners and business owners as equivalent ignores the fundamental differences in how their income is generated and the ongoing obligations they face.

Regarding who pays what, we responded to a similarly misplaced comparison a few years back but it’s worth revisiting. The CRS report identifies Section 199A as an advantage but ignores a long list of tax benefits enjoyed by employees, including employer-provided health insurance and employer-paid retirement contributions. Employees also get half of their payroll taxes paid by their employer.

Pass-through owners, on the other hand, pay the full SECA tax and have less access to tax-advantaged benefits. When they do get those benefits, well, they are the one paying for them, aren’t they? Take all that into account and the advantage conferred by Section 199A simply disappears. In many scenarios, the business owner pays a higher effective rate, even with 199A.

The real world bears this out. Many experts worried (see here, here, here, and here) 199A would lead to a wave of employees quitting their jobs to become independent contractors. IRS data and independent studies make clear that never happened. For example, here’s the key passage from a 2021 NBER paper:

Taken together, our analyses of contractor transitions show no evidence of a short-run increase in independent contracting as a result of Section 199A…nor do we see a rise in individuals becoming contractors (or forming other sole proprietorships) more generally. Thus, using several measures, we do not find any evidence that Section 199A has led to increased contractor work relative to wage employment.

Finally, we should emphasize that this is all beside the point. The local hardware store owner doesn’t compete with his employees, he competes with Home Depot. That is the horizontal equity question that should challenge the experts – how do you ensure that Main Street businesses paying 37 percent top rates are not disadvantaged when competing against their larger, public competition paying just 21 percent?

The answer is 199A. As our EY study makes clear, with it there’s rough parity. Without it, public C corporations will continue to use their tax and financial advantages to accelerate the economic consolidation already taking place across the country – raising cheap capital, buying successful family businesses, and stripping our communities of the economic power and vitality they need.

SALT Parity 2.0

One BIG Main Street win in the One Big Beautiful Bill (OB3) was what didn’t happen: Congress rejected ill-considered proposals in both the House and Senate drafts to limit pass-through entity (PTET) deductions for state and local taxes (SALT).

That was huge for many reasons, but primarily because the C corporation down the street continues to fully deduct their SALT. In what rational world is Home Depot allowed to deduct its SALT, but your local hardware store is not?

In place of limiting PTET deduction, Congress instead voted to temporarily raise the individual SALT cap from $10,000 to $40,000. What impact does that have on state PTET laws, particularly for smaller pass-throughs? Here’s what S-Corp President Brian Reardon recently told Law360:

“Treating PTET as a business expense helps ensure business owners get deductions for 100% of the taxes they pay,” he told Law360. “It can also simplify their returns by consolidating all those tax payments.”

Reardon said the new law levels the playing field for pass-throughs with their C corporation competition on SALT, but the group plans to push for greater use of PTETs.

So Treasury blessed PTET deductions back in 2020, and now Congress has elected to leave them in place following a rigorous debate. That’s good news for the Main Street community and it begs the question – what’s next for our SALT Parity efforts? Here’s the plan.

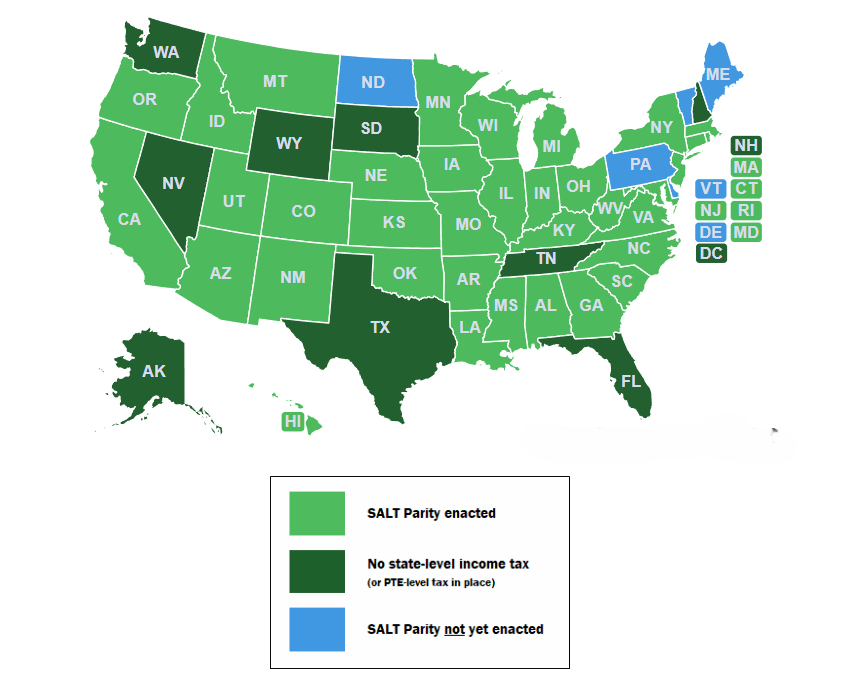

First, we need to finish the job. Through our Main Street Employers Coalition, we successfully enacted SALT Parity statutes in three dozen states, unlocking around $20 billion in savings for pass-through businesses each year.

Businesses in states that have failed to act, however (Pennsylvania, North Dakota, Vermont, Maine, and Delaware), remain at a disadvantage, unable to claim the same full SALT deduction available to their competitors. This makes no sense, so we will start by getting SALT Parity enacted in those states.

Our next priority will be to ensure that existing PTET laws are made permanent. A number of state PTET laws – including California, Illinois, and Oregon – were either tied to the federal SALT sunset or are otherwise scheduled to sunset next year. Absent action, employers in some of these states could lose access to their PTET deductions even as federal rules continue to allow them.

Third, we need to improve or fix some existing PTET laws. While most SALT Parity laws enacted in recent years follow the basic framework outlined in our initial 2018 model legislation, every law is different and some states added provisions that needlessly limit the deduction:

- In Oregon, the Department of Revenue disallows the PTET election if a trust owns any portion of the business, effectively excluding many family businesses from participating.

- In Maryland, recent changes have jeopardized S corporation eligibility and will need to be fixed.

- In California, businesses must pre-pay 50 percent of their anticipated PTET liability early in the tax year, resulting in liquidity challenges for many businesses.

- Many states made the election process needless complex and/or difficult. Our model bill argued for annual elections made when the business submits its tax return. That’s still the best approach.

Finally, we will work in Washington to make sure PTET deductions benefit real businesses only and are not used as a tax dodge or a tool for states to raise revenues at the expense of the federal taxpayer. During the OB3 debate, concerns were raised regarding the potential misuse of PTET deductions. We address many of those, but there remains the potential for states to take advantage (looking at you, Massachusetts). We plan to work with Congress to address that.

The bottom line is OB3 preserved SALT Parity for pass-through businesses and opened the door for us to move on to the next step – finishing the map and improving the rules so Main Street business owners can fully benefit from this hard-won victory.

The Assault on Privacy Continues

Treasury’s rollback of the wildly overbroad Corporate Transparency Act (CTA) reporting requirements was a major step in protecting the privacy of Main Street business owners, but it’s not the only threat out there.

New mandatory country-by-country (CBC) reporting for multinational enterprises (MNEs) operating in Australia marks a radical departure from established practices by forcing private enterprises to expose commercially sensitive and personally linked information to the public domain. The regime is disproportionate, intrusive, and constitutes a violation of the privacy of the businesses and the individuals who own them. As PWC notes:

The Australian Parliament has passed legislation that will introduce public country by country (CBC) reporting obligations with effect from 1 July 2024. This will require large multinational groups with an Australian presence to submit data on their global financial and tax footprint to the Australian Taxation Office (ATO), which will be made available publicly. This new obligation will apply in addition to existing confidential CBC reporting regime and any other public CBC reporting regime that a multinational group may be subject to (e.g. the European Union regime).

The new rules require MNEs to publicly disclose detailed financial and tax-related data for each jurisdiction in which they operate—including profit before tax, income tax paid, related party transactions, employee headcounts, and tangible assets. Unlike the OECD’s disclosure regime, this version goes further by publishing the information on an open-access register.

In the hands of competitors, political activists, or hostile foreign states, this data is not benign. For privately held MNEs, especially family-owned or closely held firms, the disclosure of this information is tantamount to a forced forfeiture of their right to privacy.

The key here is the new rules apply to public and private companies alike. Many multinational firms affected by this regime are private companies, not listed on stock exchanges. These entities are not subject to market disclosure rules precisely because they are privately owned and do not seek public capital. Australia ignores this distinction, and the result is the publication of information rivals can use to reverse-engineer business strategies, margins, resource allocations, contractual relationships and pricing.

Worse, the data cannot be divorced from the individuals behind the companies—a point of particular importance in the United State where the pass-through model is so prevalent. In many jurisdictions, corporate and tax data is linked to Beneficial Ownership (BO) registers. Public CBC data makes it easier to track wealth, investments, and earnings of private individuals. Owners or executives of firms operating in controversial sectors may face heightened risks of targeting, harassment, or extortion. It’s not just a tax transparency measure—it is forced public exposure of US citizens operating private businesses.

As with the CTA, Australia has failed to justify this massive data collection operation. The government has provided no clear evidence that privately held MNEs in Australia are engaging in widespread base erosion or tax abuse that justifies public reporting. Meanwhile, existing tools—like the OECD’s CBC reporting, transfer pricing documentation, and targeted audits—already provide Australia with extensive oversight.

Requiring reasonable disclosure of pertinent information to tax authorities is a key aspect of the tax collection process, but those rules need to be balanced with fundamental protections of privacy. Tax information submitted to the IRS is highly protected for a reason, and the few leaks we’ve seen of IRS data have received widespread attention for the very reason that they threaten the very foundation of our tax collection system.

Australia’s CBC reporting rules trade the privacy of companies and individuals for a political gesture—one that aligns with activist rhetoric rather than balanced governance. In its place, Australia should revert to confidential CBC reporting aligned with OECD standards, protect privately held firms from unnecessary public disclosures, and introduce safeguards to prevent the misuse of the published data.

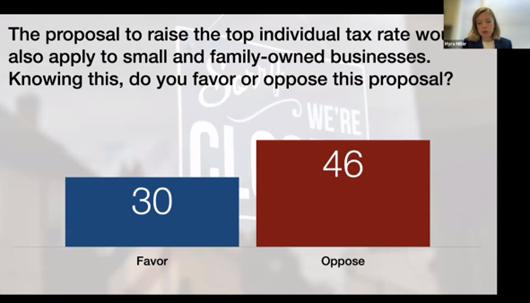

Webinar Recap: OBBB Resonates with Voters

Earlier today, S-CORP hosted a webinar featuring David Winston and Myra Miller of The Winston Group, longtime experts in measuring voter attitudes on tax policy. The focus was the One Big Beautiful Bill and its Main Street tax provisions, which are not only good policy but also extremely popular with voters.

So how popular are these provisions?

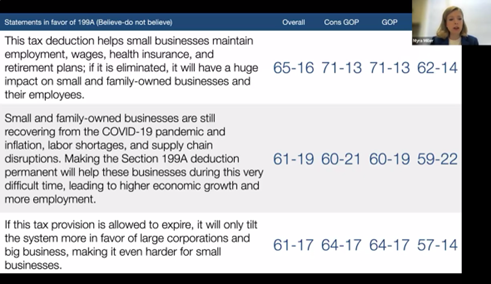

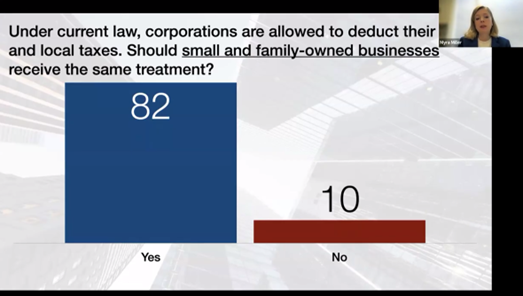

Very. The Winston Group’s research shows broad, bipartisan support across key items in the bill. For example, Section 199A continues to enjoy strong favorability, with 60 percent of voters supporting the deduction outright, and even stronger support when they learn how it helps small businesses create jobs and compete.

Similarly, when voters were presented with the idea of restoring SALT parity for pass-through businesses, support increases significantly, especially when it’s framed as a matter of fairness with C corporations.

The presentation also highlighted how Main Street remained front and center throughout the tax debate. While some voters express openness to higher taxes on the wealthy, that support collapses when they learn that many “high-income earners” are actually small and family-owned businesses. As David and Myra made clear, voters overwhelmingly believe that Main Street businesses should pay less in taxes, not more.

The takeaway? These Main Street provisions aren’t just sound economic policy, but also resonate with broad swaths of the American electorate. Lawmakers should be talking about them loudly and often as they head into August.

For those interested in learning more, click here to access the full recording!

What’s Next for 199A?

Enactment of the Big Beautiful Bill was a big beautiful win for Main Street – making permanent the lower tax rates, 20-percent deduction for small and family-owned businesses, and the higher estate tax exemptions. All these provisions help pass-through businesses compete with their larger, publicly-owned competition and they help to protect the 2.6 million jobs that depend on the 199A deduction.

With the bill signed into law, what’s next? This from Bloomberg:

“Everyone’s been coming off the momentum, because we’ve had a lot of wins, and so I think that’s what’s been pushing this idea that we’re going to maybe do a second reconciliation bill,” Curtis Beaulieu, senior policy adviser to Johnson, speaking at an event organized by accounting giant Ernst & Young…

A future bill could include tax measures that didn’t make into the package signed into law, like increasing the passthrough business deduction under Section 199A to 23% from 20%, he said.

So what might 199A 2.0 look like? Here are some ideas:

23 Percent: As Bloomberg notes, the House-passed reconciliation bill sought to bump the 199A deduction by three percentage points. Over 120 Main Street trade associations backed the proposal, citing the economic benefits the change would bring, as well as the need for a more generous deduction amid other longstanding tax hikes squarely targeted at pass-throughs. While that proposal was left out of the final bill, it’s clear there’s support both on Capitol Hill and within the business community for expansion.

Foreign Income: As part of Chairman Smith’s Tax Teams exercise last year, we submitted comments that touched on the inequitable treatment of foreign-source income earned by pass-through businesses. While C corporations are permitted to deduct a significant portion of their foreign earnings and otherwise enjoy favorable treatment under the GILTI regime, pass-throughs are excluded from territorial treatment and pay rates up to 37 percent on their overseas income immediately — without the benefit of the 199A deduction. This discrepancy discourages global investment by American pass-throughs and puts them at a competitive disadvantage when doing business abroad. A future tax package should allow qualified foreign business income to receive the same 199A deduction as domestic income.

199A Deficit Accounts: As we noted earlier this year, current law prevents many pass-through businesses from accessing the 199A deduction due to so-called “199A deficits” — losses incurred in prior years that must be fully recouped before the deduction becomes available again. This restriction has proven especially punitive for businesses that took losses during the pandemic in order to keep their employees on payroll and operations running.

Now that many of these businesses are back in the black, they find themselves unable to benefit from 199A until they run through all their accumulated losses. C corporations, by contrast, face none of these obstacles. NOLs generated by C corporations apply broadly to all income and allow them to reduce taxable income without limitation, all while benefiting from a flat 21 percent rate. Pass-through businesses operate under a far more restrictive regime, with narrower deductions and tighter eligibility rules.

To address this challenge, we proposed a one-time election to wipe out existing 199A deficit balances, enabling affected businesses to immediately reclaim the deduction. This simple change would help businesses harmed by the pandemic and restore the original promise of 199A, ensuring it remains a reliable source of tax relief for millions of family businesses.

Eliminate the SSTB Designation: Another unique feature of the 199A deduction are the so-called “guardrails” that limit its application above certain income levels. Generally, if a business owner’s taxable income exceeds about $500,000, they don’t get the 199A deduction benefit if they are in the wrong industry (professional services) or if they don’t have significant levels of employees and/or investment. According to Treasury, these guardrails have a significant bite and reduce the 199A benefit by about 40 percent.

S-Corp supports some of these guardrails. For example, we first proposed the wage and investment limitation as a means of ensuring the 199A benefit goes to real businesses with real employees and investment. As a business owner, if you don’t create jobs and invest in your community, you don’t get the 199A deduction. Critics of 199A completely ignore this aspect of the law.

The exclusion of certain industries (Specified Service Trade or Business, or SSTB), on the other hand, is an extraordinarily bad policy. Why should a manufacturer with 500 employees get the 199A deduction but an accounting firm with 500 employees is excluded? Don’t accounting jobs matter too? Superficially, the SSTB designation was to prevent professionals whose income derives primarily from their own efforts from getting the deduction, but we already solved that challenge with the wage limitation. Only lawyers and accountants that create jobs get the deduction. The SSTB provision does nothing but punish some business owners because they are in the wrong industry.

With the BBB behind us, it’s time for Congress and Main Street to start the discussion of what comes next. An improved 199A deduction needs to be part of that discussion.