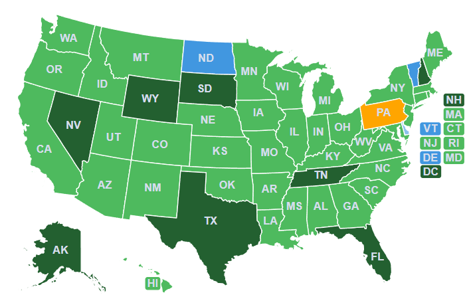

Lots to report on the SALT Parity front. As you can see from our map, the number of states adopting our PTET elections is up to 38, with only four to go. It’s not all good news, however, as some states are considering backsliding on the policy while others are using the PTET regime to offset significant new taxes. Here’s the rundown.

Back in March we flagged an emerging threat to New York’s Parity regime, noting that their budget proposals included PTET “haircuts” that would siphon money away from New York’s Main Street businesses and into state and city government coffers.

The proposal included cutting the state PTET credit to 90 cents on the dollar, while Mayor Mamdani went further, requesting the state reduce the city credit to 75 cents. Fortunately, Governor Hochul opposed the proposal and, more recently, announced both haircuts were left on the cutting room floor. The existing PTET regimes in New York State and New York City remain intact.

So a good result, but not exactly a clean bill of health. The episode revealed the dark underbelly of SALT Parity — when states face a budget crunch, they often view our PTET credits as an opaque means of raising revenue.

Maine is a good example. The state enacted our SALT Parity reform just this spring, but the new PTET includes a 10 percent haircut diverting funds away from businesses and into the state’s coffers. Also included was a 2 percent income surtax on individuals above $1 million, a so-called “millionaire tax.” Taxpayers subject to the new tax will pay an extra $20,000 in state taxes for every million they earn, while splitting the new PTET credit $6,660/$740 with the state. Not a great outcome for Main Street. That’s a net tax hike for taxpayers subject to the surtax, and a smaller than expected tax benefit for those below it.

Washington State, meanwhile, is on its own journey. The state recently enacted its first-ever personal income tax — a 9.9 percent tax (seventh highest in the country) on income exceeding $1 million. The state had historically rejected imposing an income tax, with voters adopting an initiative prohibiting one as recently as 2024. That initiative means the new tax faces an inevitable legal challenge, but the Washington State Supreme Court is highly flexible and likely to embrace the new tax anyway. Bottom line, as with Maine, the enactment of the new PTET regime in Washington is a one step forward, two steps back proposition.

On the brighter side, several states have moved to extend and/or improve their PTET regimes. California extended its SALT Parity program through 2030 as part of last year’s budget and added flexibilities around election timing and payments to reduce administrative burdens. Elsewhere, Minnesota and Oregon passed extensions of their programs through 2027, while Illinois took the strongest step by making its PTET law permanent late last year. It’s a welcome contrast to the erosion we’re seeing elsewhere, and a reminder that SALT Parity shouldn’t be treated like a piggy bank.

Finally, we will ask again — what are North Dakota, Pennsylvania, Delaware and Vermont waiting for? As we’ve said from the beginning, SALT Parity is a rare win-win for states. It costs the States nothing, while their Main Street businesses get a restored business deduction. For lawmakers in those states, they are leaving billions in tax savings on the table.

SALT Parity is one of the more tangible policy wins Main Street has achieved in recent years, and we oppose efforts to quietly erode it through haircuts or other backdoor tax hikes. We’ll keep tracking (and fighting) these threats even as we vigorously wave the SALT Parity flag.