The Brookings Institution is out with two new tax studies, one great, one not so much.

The great one is a paper by Bill Gale, Adam Looney and Elena Patel calling for a border-adjusted cash-flow tax. This is something S-Corp supported when it was debated in Congress back in 2016, and it’s still a good idea. Why? It would balance out tax rates between industries and financing methods, it would eliminate the need for all those ridiculous international rules, and it would fit nicely into a corporate integration regime that would level the playing field for close-held businesses and their publicly owned counterparts. As the Tax Foundation noted back in 2016:

Corporate integration would accomplish many of the same goals as a corporate rate cut, such as making the U.S. business climate more competitive. It could also end several economic distortions created by the current tax code, including the tax preference for debt financing over equity financing.

It would also raise beaucoup bucks that could be used to reduce taxes elsewhere. Here’s the key graph:

This package would increase investment, simplify the corporate tax, reduce distortions, and raise revenue in a progressive manner. The authors estimate that, taken as a whole, the proposal would raise over $4.7 trillion over 10 years. Even without the border adjustment, the domestic reforms alone would raise about $1.5 trillion over 10 years and make the corporate tax system simpler and more efficient, although they would not address profit shifting or international rate competition.

The border adjustment is key, as it ensures that products produced in the US are taxed in a similar manner to those produced elsewhere. It converts the corporate tax from a tax on domestic production to a tax on domestic consumption such that it doesn’t matter where a product is produced – if it’s consumed in the US, the tax treatment is the same.

So a nice addition to the tax reform discussion.

On the less good side of things, however, there’s another new paper cheerleading rate hikes on Main Street under the premise that the “U.S. tax system raises insufficient revenue to meet national needs.” Apparently, large pass-throughs are to blame.

The citation for this assertion is a Tax Law Center paper offering a general critique of the OB3. Missing is a recognition that 1) tax collections are above their fifty-year average and growing, 2) the tax code is more progressive than it’s been in the past, and 3) the amount of fraud embedded in federal spending projections is simply breathtaking.

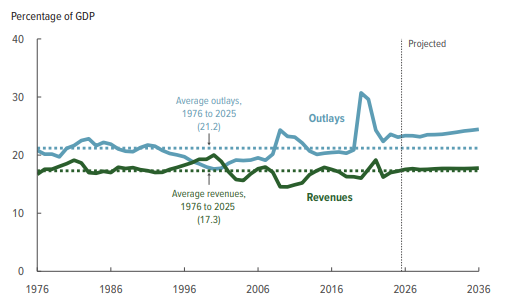

In just the last week, we’ve learned that over a quarter of Affordable Care Act enrollees are getting improper subsidies, while the GAO is out with a new report estimating improper federal payments in 2025 were $186 billion. This chart from the CBO illustrates the challenge nicely – revenues are slightly above their historic levels while spending is way higher and rising sharply.

Given all that, a mantra of “Let’s raise taxes on family businesses so we can pay for more fraud” doesn’t seem like a winning argument. Nonetheless, that’s where we are.

For S-Corp readers, the paper’s arguments will be familiar. The business tax base has eroded (it hasn’t), large S corporations pay less tax than large C corporations (they don’t), and the business community would pay more taxes if we just forced everybody back into the pre-1986 corporate tax structure (they wouldn’t).

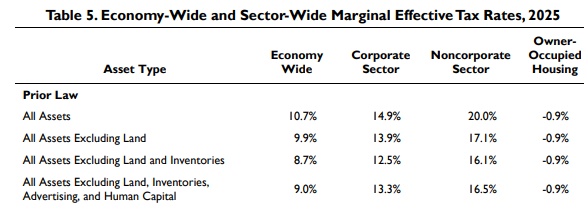

There’s too much to address in a single post (if you’re interested, we cover most of this here) but a simple reassertion of who pays what seems appropriate. Here’s the Congressional Research Service on marginal effective tax rates from last year:

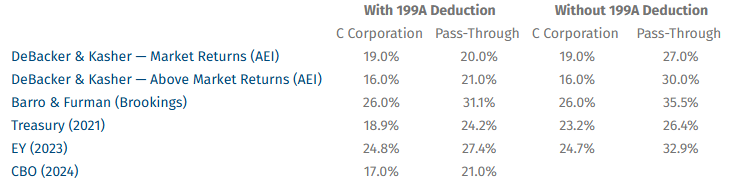

Here’s our study by EY’s Robert Carroll on how the 199A deduction affects effective tax rates:

And here’s a snappy table we put together with other sources:

What do they all have in common? They generally estimate that relative rates for pass-throughs and C corporations are similar with 199A, but pass-throughs pay more without it.

Given that most jobs are located at pass-through businesses, that’s an important observation that should instruct the direction of tax policy. The Brookings folks are correct that we face serious fiscal challenges, but casting the pass-through sector as a scapegoat based on rehashed, incorrect arguments is not going to solve the problem.