SALT Parity State of Play

Adoption of the Working Families Tax Cuts Act last July was a huge win for Main Street – a win that included locking in $20 billion of annual savings through our SALT Parity efforts. With the SALT cap now permanent, those parity laws enacted in 36 states are more important than ever.

Just as important – making sure the benefits are broad and stay in place. That means making certain that states and other jurisdictions don’t game the policy, that the laws are working as they should, and that we complete the map. Here’s the state of play on those three fronts:

State Games

Massachusetts has a PTET election, but it pairs the election with a 10 percent haircut of the state’s PTET tax credit. That haircut effectively diverts tax benefits from pass-throughs (and the federal taxpayer) to the Massachusetts state coffers. Not good.

Now the new Mayor of New York City is proposing to do the same with the NYC PTET credit, only on a whole new level. Under the proposal, New York City businesses would see their tax credit – which exists alongside the statewide credit – reduced from 100 cents on the dollar to 75 cents, a change the Mayor’s office estimates would raise around $700 million. That’s a massive tax hike, and one that would hit eligible businesses of all sizes, not just “the wealthy.”

Fortunately, Mamdani cannot accomplish this unilaterally, since modifying the credit requires Albany’s approval. But there’s a deeper concern with the precedent being set. Massachusetts showed states they can erode SALT Parity by quietly pocketing a slice of the benefit, creating a template others may be tempted to follow.

Sunsets & Fixes

Our SALT Parity bills include three key components – an election to pay at the entity level, offsetting credits or income exclusions to avoid a double tax, and a recognition of the credits or income exclusions offered by other states.

Beyond that common core, every Parity bill is different, reflecting the unique nature of each state’s tax code and the preferences of its legislators. We attempted to summarize those differences in this table.

One key difference is that a handful of states sunset their Parity laws to coincide with the original 2026 expiration of the federal SALT cap. S-Corp advised against those sunsets, as the election can be beneficial even without the SALT cap, but we didn’t always prevail. By our count, six states sunset their laws. Here’s the latest on those states:

- California (2026): As part of its 2025-26 budget, extended its SALT Parity law through 2030.

- Illinois (2026): Its SALT Parity law was made permanent thanks to legislation passed in December of last year.

- Virginia (2026): Last year’s budget bill extended the expiring provision, but only for one year (through 2026). The state will need to take up the issue again this year.

- Oregon: SB 1510 – which extends the state’s “PTE-E” program – was approved by the legislature and currently awaits the Governor’s signature.

- Minnesota (2026): Legislation (HF 3127 / SF 3405) would revive the state’s defunct (expired at the end of 2025) SALT Parity regime through 2029. The bill enjoys bipartisan support, but remains stalled in the House due to larger divisions.

- Utah: No legislation introduced yet to reinstate the expired provision

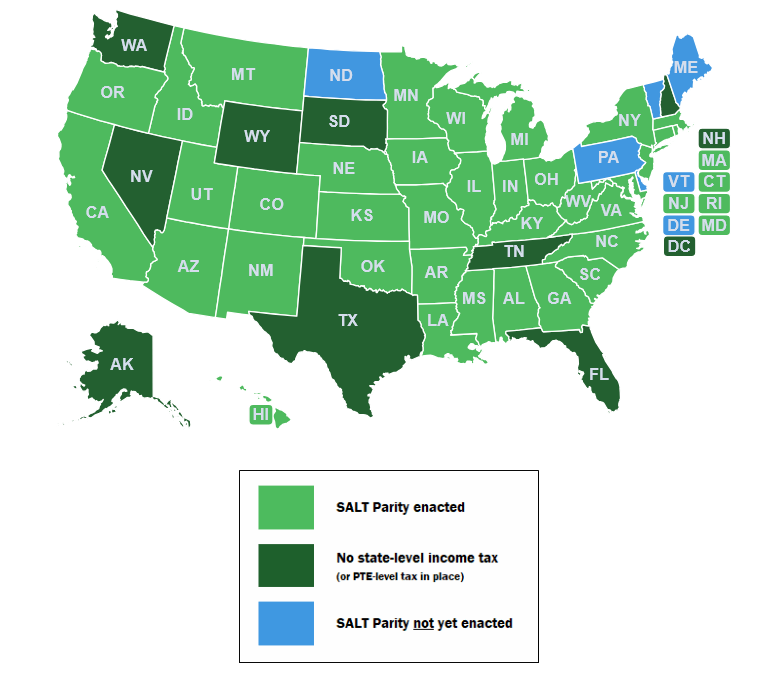

Completing the Map

Finally, not every eligible state has enacted their SALT Parity reform. Maine, Vermont, North Dakota, Delaware, and Pennsylvania are the last holdouts, leaving pass-through businesses in those states at a real competitive disadvantage – a disadvantage that’s increasingly hard to justify as the reform effort has matured. Two notable developments in those states:

- Pennsylvania: SB 659 was introduced last session and its sponsor, Senator Mastriano, has committed to reintroducing it this year.

- Maine: LD 191 was introduced last year and remains pending.

So some movement, but really a remarkable lack of alacrity for enacting a policy that puts money in the pockets of local businesses without costing the sponsoring state anything. Meanwhile, nothing is happening in the remaining states. Apparently, pass-through businesses in Vermont (21 thousand), Delaware (45 thousand) and North Dakota (30 thousand) just don’t count.

Conclusion

So that’s the latest on the SALT Parity front. We’ll continue working with lawmakers in the holdout states to enact additional SALT Parity bills while also working to ensure existing regimes remain intact and operate as intended. With the federal framework now settled, it’s time to finish the map, block attempts to hijack the policy, and lock in this relief for good.