Webinar Recap: Voters, Taxes, and the Midterms

As we head into the midterms, longtime S-CORP allies David Winston and Myra Miller of The Winston Group joined us to walk through their latest polling on tax policy, spending, and where the voters stand heading into the next big tax fight.

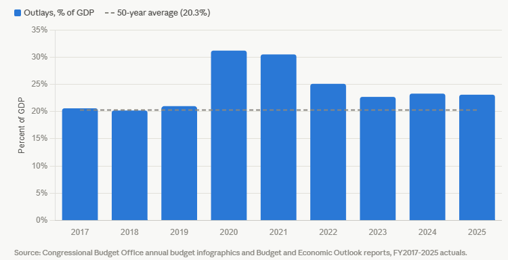

With concerns over debt, deficits, and Social Security’s pending insolvency mounting, the Winston Group’s research suggests Main Street enters the debate from a position of strength, but only if we build a foundation of understanding upon a number of key economic realities.

As we’ve covered before, when voters are …

(Read More)

{kind=link}