One of the narratives Main Street needs to counter is that the tax cuts enacted in 2017 and 2025 are depriving the federal government of necessary revenue. As our friends at the Winston Group make clear in a recent video, revenues from individuals and corporations alike are up sharply, even when inflation is taken into account:

Here’s what they say in the accompanying write-up:

- From 2017 to 2025, revenues to the federal government increased 58%. Inflation increased 31% over that same timeframe, but revenues increased at almost twice the rate as inflation.

- Individual income tax revenue increased 67%.

- Corporate tax revenue increased 52%. With the lower corporate tax rate from the 2017 Tax Cuts and Jobs Act, US companies came home and we are seeing a remarkable increase in revenues coming from corporate taxes.

- Despite the positive trends in revenues, government spending has gone up 76% in the same time period, outweighing the benefits of the increased revenues.

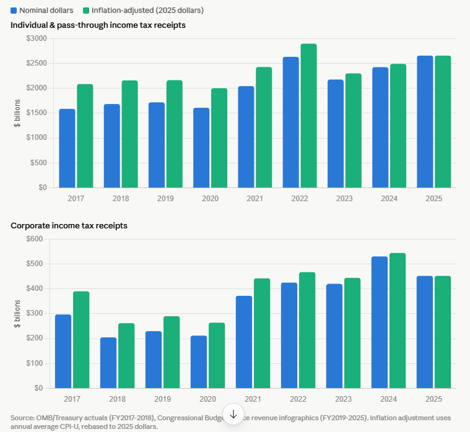

This graph from Claude illustrates the point – revenues from corporate and individual tax collections are up sharply since 2017, even when robust inflation levels are taken into account:

A few items worth flagging:

- Individual & pass-through receipts roughly doubled in nominal terms from 2017 to 2025, driven largely by wage growth and a surge in investment income in 2021–2022. As we noted at the time, the individual and pass-through revenues never dropped post-TCJA, as the lower rates, increased deductions and credits, and more generous expensing provisions were largely offset by the bill’s expansive base broadening.

- Corporate receipts, on the other hand, fell sharply in 2018 due to the lower corporate rate and new expensing rules. By 2024, however, that decline had fully reversed with collections coming in at well over $500B before OB3’s restored expensing provisions pulled 2025 receipts back down. You can try to argue that lower rates and faster capital depreciation don’t encourage investment and growth, but it’s kind of staring us in the face here, no?

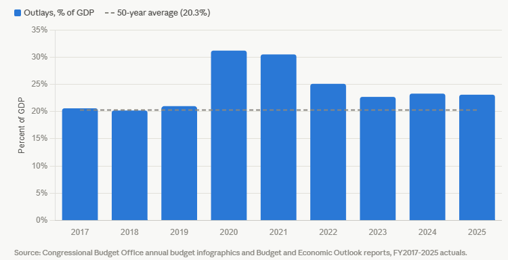

So, federal revenues post-tax cuts are strong and growing. How about spending? Has it been reigned in post-COVID? No:

As the chart shows, federal spending is well above the 50-year average and continues to claim a bigger share of the economy than it did pre-COVID:

- Years 2017–2019 were close to the 50-year average of 20.3% — spending wasn’t historically elevated heading into the pandemic.

- FY2020–2021 are the outliers at over 30 percent of GDP, a level of spending not seen outside World War II.

- Since then, spending has settled into the 22–25 percent range, still meaningfully above the 50-year average. Notably, spending in 2025 is barely different from 2022, showing the “structural” elevation in spending that took place during the pandemic.

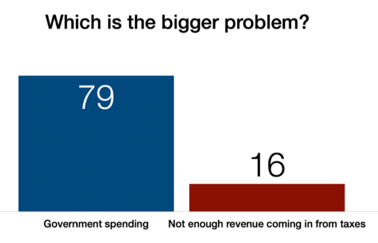

Bottom line – federal tax collections are historically high and continue to grow at robust rates, but federal spending is growing even faster and is simply unsustainable. This explosion of spending has been noticed. As our Winston friends point out, “The electorate believes the larger cause of the deficit is spending too much rather than taxing too little.”

The electorate is correct.

The electorate is correct.