While most people were trying to file their taxes last month, Senator Elizabeth Warren was busy trying to raise them. Her reintroduced Ultra-Millionaire Tax Act of 2026 would impose a 2-percent annual levy on individual net worth above $50 million, a 3-percent rate on billionaires, and generate what its proponents claim will be over $6 trillion. That estimate is the economist equivalent of drawing blood from a stone – it doesn’t exist and it shouldn’t be taken seriously.

Warren’s latest proposal also includes a 40 percent “exit tax” on the net worth of any American worth more than $50 million who renounces their citizenship. The message, delivered with all the subtlety of Sonny locking the bar door in A Bronx Tale, is unmistakable: “now you can’t leave.” Setting aside the enforcement and constitutional issues, we would again point out that forcing people to stay is hardly the foundation of a healthy relationship. It is what totalitarian governments do, not democracies.

Back to the revenue estimate, the $6.2 trillion figure comes from Berkeley economists Emmanuel Saez and Gabriel Zucman, the same duo who have animated every version of this wealth tax since 2019 (and whose wildly inaccurate claims we’ve covered for even longer).

In terms of methodology, they start with the Forbes real-time billionaire list, assume an annual wealth growth rate of 4 percent, slap on an arbitrary 15 percent haircut for “evasion and avoidance,” and call it a day. If that approach sounds familiar, it should. Saez used the same “back of the envelope” approach for his estimate of the California wealth tax initiative.

These rough estimates are a poor substitute for reality. They ignore any behavioral responses and assume the economic landscape will look the same after the tax as before. In this fantasy world, the federal government seizes two to three percent of high-net-worth capital every year but nothing changes – the capital remains in place, businesses remain structured as they are now, and entrepreneurs keep building wealth at the same rate. Sure.

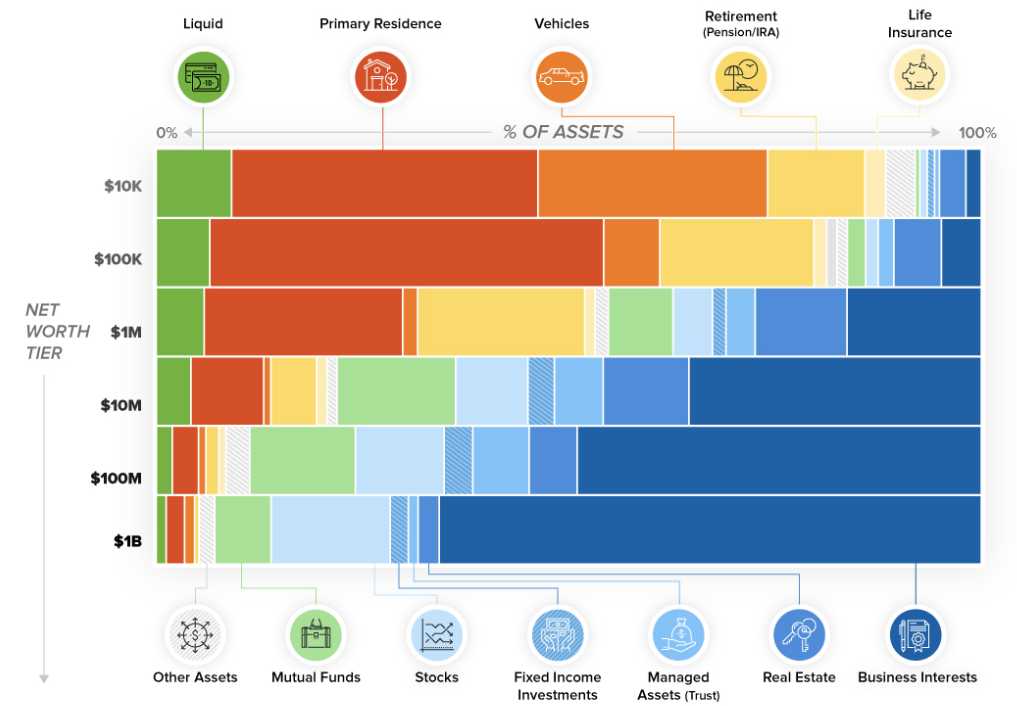

One challenge among many — most of the assets held by wealthier Americans are not sitting in a brokerage account, waiting to be liquidated. Rather, they are in the form of equity in enterprises that, cumulatively, employ millions of people. The dark blue area in this Visual Capitalist chart reflects illiquid business assets subject to tax under the Warren bill. In effect, the federal government becomes a preferred shareholder in every one of those enterprises, extracting an annual dividend whether the business makes money or not.

For example, the Warren tax would impose an annual $3 million tax bill on the owner of a $200 million manufacturing operation. This comes on top of income taxes, so if the company earns a 6 percent return on its assets – a very respectable return – then the income tax would take about 2 percent and the wealth tax another 1.5 percent.

That leaves the owner with an after-tax return of just 2.5 percent (not respectable) and wondering where else they can invest their capital. The “just two cents” framing Warren deploys to sell her tax is really a 62 percent confiscatory tax, and that’s under the best of circumstances.

What if the company loses money? How does the tax work then? It’s simple — the owner still owes $3 million. Without any income, they have to dip into their savings or borrow against the (declining) value of the business. To be clear, this is not a public company where shares are easy to value and sell. Borrowing for closely-held businesses is much more involved. And there are limits — what if the company is already fully leveraged?

Now take the negative effects this tax has on this one company and multiply them across the 260,000 households Warren’s bill targets. It’s easy to see the behavioral response will not be negligible but very, very robust. Just ask California, New York, Washington, the UK, Spain, Norway, and other jurisdictions experiencing rapid outmigration.

Warren’s bill will not pass this Congress, but the proposal does not have to become law to do damage. As with the California initiative, the threat alone accelerates restructuring, departures, and capital flight. In the end, the disruption to business and investment will be higher than expected, and the revenue raised will be lower than advertised. As the adage goes, you can’t draw blood from a stone.