Bad Data

Jack Salmon, Research Fellow at the Mercatus Center and author of the Substack The Unseen and The Unsaid (and recent podcast guest!) has a great piece out this week that tears down the myth popular among tax hike advocates these days.

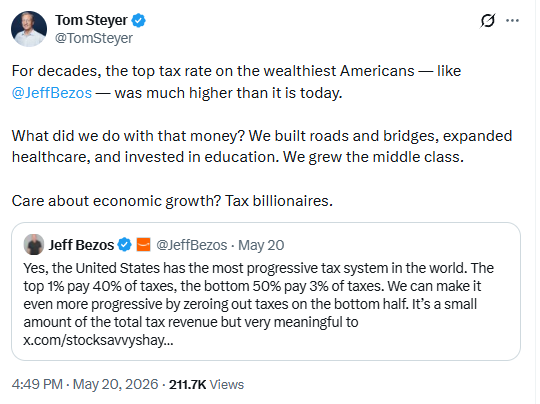

The writeup was inspired by a post on X from Tom Steyer, billionaire and California gubernatorial candidate, making a familiar argument: top tax rates were sky-high in the postwar decades, and all that revenue built the middle class.

This claim surfaces reliably in every tax debate, deployed to suggest that returning to 70 or 90 percent rates would solve all our fiscal woes. Salmon takes that logic apart:

In 1952, the federal government raised 18 percent of GDP in tax revenues. This compares with federal revenues of 17 percent of GDP today. So, relative to today, “all that money” amounted to only about 1 percent of GDP in federal revenue, roughly $300 billion in today’s economy, or about 2 weeks of current government spending.

On the spending side, Steyer credits those high-rate decades with building roads, funding health care, and investing in education, but the numbers don’t line up.

…Adjusting for inflation, in 1979, the federal government spent $222 billion on all health care programs. Compare this to the FY 2025 budget which allocated $1.66 trillion to Medicare and Medicaid combined, or more than 7-times the amount in 1979.

…For transportation and education spending in 1979, the federal government spent roughly half as much on both as it does today, adjusting for inflation. Even if we adjust for population growth, the federal government still spends significantly more today on transportation, education, and especially on health care.

In other words, the spending buildup happened after rates fell, not during the era of confiscatory rates.

But the most revealing data in Salmon’s piece concerns effective rates, what the wealthy actually paid versus what the statute said:

In 1952 when the top income tax rates were 92 percent, the top 1 percent paid an effective rate of less than 17 percent, while the top 0.1 percent paid a 21 percent effective income tax rate. Today, both the top 1 percent and 0.1 percent pay effective income tax rates above 26 percent. So, with a top rate of 37 percent, the wealthiest Americans pay higher effective income tax rates than they did with a top rate of 92 percent.

The reason is straightforward. The mid-century tax code offered a menu of alternatives. Wages faced a 92 percent rate, corporate income was over 50 percent, and capital gains 25 percent. Naturally, taxpayers took their income in whichever form was cheapest.

We’ve covered this dynamic before (see here and here). Taxpayers in that era simply routed their income through corporations and capital gains to avoid the top brackets entirely, assisted by a complex web of deductions and workarounds that made the avoidance more tolerable. This CBO heatmap below makes the pattern visible:

The dark upper bands (rates above 50 percent) cover only a thin sliver at the very top of the chart before largely disappearing as rates came down. The color that dominates across the whole period is yellow, the lower brackets. The exception is the inflationary 1970s, when bracket creep pushed ordinary workers up the rate schedule. That is when the upper bands briefly widened. The top rates raised revenue in that decade by taxing the middle class, not the wealthy.

Taxpayers revolted. The inflation-fueled bracket creep of the 1970s sparked the Reagan Revolution, drove rates down, and produced indexed brackets. The result was a more friendly, progressive tax code – rates came down for the middle-class and the wealthy shouldered a higher percentage of the tax burden.

Ironically, today’s leading advocates for higher wealth taxes often acknowledge this dynamic, albeit inadvertently. In an NYT op-ed backing California’s proposed billionaire wealth tax, Berkeley economists Emmanuel Saez and Gabriel Zucman repeatedly describe how wealthy taxpayers restructure income, relocate, and otherwise respond to tax incentives. The piece spends multiple sections rebutting concerns about billionaires leaving California, while simultaneously documenting how many have already begun “making moves to leave the state.”

That’s the entire point. The history of the 90 percent era was never one of the wealthy dutifully paying confiscatory rates. It was one of avoidance and behavioral response. Salmon’s piece strips away the mythology and focuses not on headline rates, but on what taxpayers actually paid.

Billionaire Brake Check

Jeff Bezos sat down with CNBC’s Andrew Ross Sorkin this week and spent the better part of an hour challenging the political dogma that taxing the rich is the answer to all our country’s economic problems. It’s worth watching, if only to see Sorkin, who specializes in interrupting his guests, barely get a word in during the entire interview.

Right out of the gate, Bezos addressed the flawed wealth inequality narrative underpinning much of today’s tax-hike movement:

What’s happening here is politicians are using… this age old technique of, you know, picking a villain and pointing fingers. But the problem is that doesn’t solve anything. And so like, if you want to help the group of people who are struggling, you have to figure out real root causes and solutions. And that takes skill.

…If you really are being honest about it, we don’t have a revenue problem in this country. We already have the most progressive tax system in the world. The top 1 percent of taxpayers pay 40 percent of all the tax revenue. The bottom half pay only 3 percent… We actually have a spending problem and that’s a skills issue.

Bezos used the New York City school system as a prime example of the challenge:

They spend $44,000 per student. That’s 30 percent more per student than other big cities like Chicago, LA, and Boston. And it’s three times more than Miami and Houston. And by the way, New York City doesn’t get better outcomes. If we ran Amazon the way New York City runs their school system, your packages would take six weeks to arrive. We’d have to charge you a $100 delivery fee. And then when the package did finally arrive, it’d have the wrong item in it anyway.

As we’ve pointed out repeatedly, federal tax revenues are currently above historic levels and the tax code is more progressive (the rich pay more) than at any time in the last 60 years. Yet some still want more – always more. At what point can we admit we have a spending problem?

Bezos also addressed the so-called “buy, borrow, die” strategy that has become a fixation of tax hike proponents in recent years:

As far as I know, there is no truth to this ‘buy, borrow, die’ thing. I don’t even know where this comes from. I’m selling Amazon stock routinely, and that’s how I fund Blue Origin and a bunch of other things. So every time I sell I pay taxes on that…I’m a little skeptical that’s a true loophole. But if it is we can fix it. But when you fix that loophole, it’s not going to help that nurse in Queens. It’s not going to help her at all.

As we wrote previously, is any tax avoidance plan in which the taxpayer has to die to benefit really that great?

One of the comments that got the most attention was Bezos’ call for eliminating taxes on lower- and middle-income taxpayers:

A nurse in Queens who makes $75,000 a year pays more than $12,000 a year in taxes. Does that really make sense? So, people talk about making the tax system more progressive. How about we start by having the nurse in Queens not pay taxes? That’s $1,000 a month that could help with rent or groceries or anything. And by the way, do you know what that all adds up to? The bottom half of income earners in this country pay only 3 percent of the taxes. It’s only 3 percent. We can find 3 percent. It’s a small amount of money for the government.

Couple problems here. One, we’ve already eliminated income taxes on families making around $75,000. The combination of the increased standard deduction and the larger child credit means a family of four earning that amount owes maybe a couple hundred dollars, while a single mom with two kids would owe only around $1,000, or $11,000 less than Bezos’ claims.

Two, the real tax burden on the middle class these days are wage taxes to cover Social Security and Medicare. In Bezos’ example, that’s likely the source of the $12,000 tax bill. But those taxes pay for very progressive benefits to the same group of people, while taxing all the billionaires on all their wealth would not cover the cost of those programs. What to do? Check out this solution.

Back to Bezos’ broader point — the federal government wastes enough money that it could afford to stop taxing lower-income earners without reaching further into anyone else’s pocket. He made this explicit when Sorkin pressed him, responding: “You could double the taxes I pay and it’s not going to help that teacher in Queens, I promise you.”

The irony that this clear defense of Main Street comes from the world’s wealthiest person is not lost on us. But the reality is that endless tax hikes are not a substitute for effective governance, and punishing capital does not help the people politicians claim to represent. S-Corp has been making that case for years. It’s nice to hear a rich guy step up and make it too.

Thune Talks Main Street Tax Relief

As part of National Small Business Week, Senate Majority Leader John Thune took to the Senate floor to highlight how provisions like permanent Section 199A, bonus depreciation, estate tax relief and other provisions from last year’s Working Families Tax Cuts are helping Main Street employers hire new workers and reinvest in their communities.

As Thune put it:

Nearly half of Americans in the private sector work for a small business. Small businesses are responsible for a majority of the new jobs in this country. And a lot of Americans’ first jobs were at a small business, mine included…There’s nothing small about the impact that small businesses have in our country.

That point often gets lost in Washington’s tax debates. Today’s tax conversations tend to focus on large publicly-traded corporations, while the pass-through businesses employing most Americans are treated as an afterthought. Thune’s remarks were a useful reminder that the Main Street economy remains the backbone of job creation and economic growth in the country.

He also highlighted the importance of making 199A permanent:

I’ve heard positive feedback on 199A across industries in my state. In South Dakota, an agricultural cooperative estimates the impact of this one policy at over $100 million since 2017 – and that money has been able to be passed on to the farmers that are members of that co-op. And I’m sure that those farmers – like so many small businesses across the country – are relieved that 199A is here to stay.

Certainty matters. For years, Main Street employers operated under a cloud that key provisions of the 2017 tax law would expire, making long-term planning more difficult while setting the stage for steep tax hikes. Permanence gives family-owned businesses more confidence to invest for the long haul.

Thune also focused on bonus depreciation and the practical impact it can have for smaller operations:

Say you’re a farmer and you need to replace your combine, or a manufacturer who needs to upgrade your machinery, or a plumber who needs a new truck. Those are all big expenses, especially for a small, maybe even in some cases, one person operation. So bonus depreciation helps small businesses take on that big expense by allowing them to deduct the entire thing in that one year, and the impact can be significant.

Tax policy is too often described through abstract budget tables and revenue estimates, but for Main Street businesses these provisions frequently determine whether an expansion, equipment purchase, or hiring decision happens at all. The examples Thune cited are familiar to businesses in every state and district.

Thune closed by pushing back on claims that the tax package primarily benefited wealthy taxpayers, pointing out that workers, family businesses, and local employers are already seeing the impact. And as we’ve seen post-tax filing season, the refund and broader relief data backs that up. That’s the story we’re going to have to keep conveying.

Main Street Supports SCOTUS Review of CTA

More than 90 trade associations sent a letter today urging the federal government to support Supreme Court review of the Corporate Transparency Act. The letter calls on Treasury and DOJ to back the two pending cert petitions currently before the Court — National Small Business United v. Bessent and Texas Top Cop Shop, Inc. v. Blanche — so that the fundamental constitutional questions raised by the CTA can be resolved once and for all.

The letter was led by the S Corporation Association and comes as the CTA faces mounting legal and political pressure from the business community. It reads:

The CTA imposes an unprecedented reporting regime on tens of millions of businesses and other legal entities, raising exceptionally important constitutional, privacy, and federalism questions warranting definitive review by the Court.

Treasury’s March 2025 interim final rule exempted domestic entities and U.S. persons from the CTA’s reporting requirements, providing welcome and meaningful relief to millions of small businesses, homeowners’ associations, and other enterprises that otherwise would have faced the challenge of ongoing CTA compliance coupled with the threat of severe civil and criminal penalties. The underlying CTA statute remains intact, however, as do the constitutional questions it raises. Only a clear ruling from the Supreme Court can put this issue to rest and prevent future administrations from reimposing the broader reporting requirements.

That last point gets to the heart of the matter. The regulatory relief the current administration has provided is real and meaningful, but it is only as durable as the administration that issued it. A future White House could reverse course and millions of small businesses would find themselves back where we started. A Supreme Court ruling would end that risk permanently.

S-Corp and its partners are pursuing the legislative route as well. Congress has the power to repeal the CTA outright, and we continue to push for that outcome. But whether the courts or Congress gets there first, the goal is the same — take this harmful statute off the books permanently.

The constitutional case against the CTA is strong, and we look forward to it prevailing in court. But first, the SCOTUS needs to add it to the docket.

Blood from a Stone

While most people were trying to file their taxes last month, Senator Elizabeth Warren was busy trying to raise them. Her reintroduced Ultra-Millionaire Tax Act of 2026 would impose a 2-percent annual levy on individual net worth above $50 million, a 3-percent rate on billionaires, and generate what its proponents claim will be over $6 trillion. That estimate is the economist equivalent of drawing blood from a stone – it doesn’t exist and it shouldn’t be taken seriously.

Warren’s latest proposal also includes a 40 percent “exit tax” on the net worth of any American worth more than $50 million who renounces their citizenship. The message, delivered with all the subtlety of Sonny locking the bar door in A Bronx Tale, is unmistakable: “now you can’t leave.” Setting aside the enforcement and constitutional issues, we would again point out that forcing people to stay is hardly the foundation of a healthy relationship. It is what totalitarian governments do, not democracies.

Back to the revenue estimate, the $6.2 trillion figure comes from Berkeley economists Emmanuel Saez and Gabriel Zucman, the same duo who have animated every version of this wealth tax since 2019 (and whose wildly inaccurate claims we’ve covered for even longer).

In terms of methodology, they start with the Forbes real-time billionaire list, assume an annual wealth growth rate of 4 percent, slap on an arbitrary 15 percent haircut for “evasion and avoidance,” and call it a day. If that approach sounds familiar, it should. Saez used the same “back of the envelope” approach for his estimate of the California wealth tax initiative.

These rough estimates are a poor substitute for reality. They ignore any behavioral responses and assume the economic landscape will look the same after the tax as before. In this fantasy world, the federal government seizes two to three percent of high-net-worth capital every year but nothing changes – the capital remains in place, businesses remain structured as they are now, and entrepreneurs keep building wealth at the same rate. Sure.

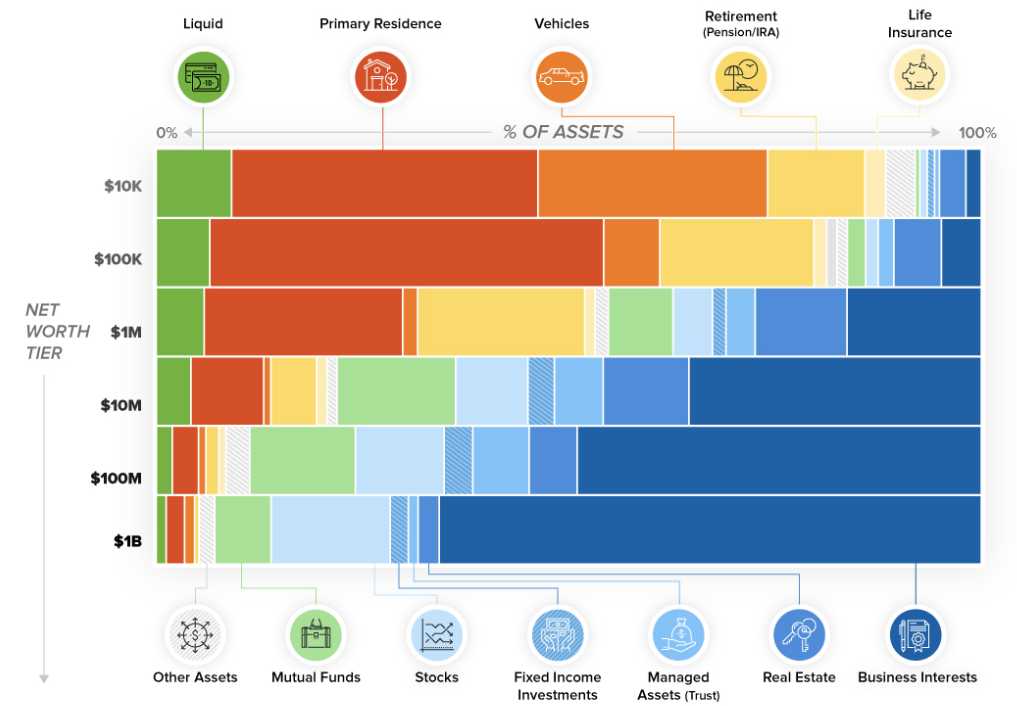

One challenge among many — most of the assets held by wealthier Americans are not sitting in a brokerage account, waiting to be liquidated. Rather, they are in the form of equity in enterprises that, cumulatively, employ millions of people. The dark blue area in this Visual Capitalist chart reflects illiquid business assets subject to tax under the Warren bill. In effect, the federal government becomes a preferred shareholder in every one of those enterprises, extracting an annual dividend whether the business makes money or not.

For example, the Warren tax would impose an annual $3 million tax bill on the owner of a $200 million manufacturing operation. This comes on top of income taxes, so if the company earns a 6 percent return on its assets – a very respectable return – then the income tax would take about 2 percent and the wealth tax another 1.5 percent.

That leaves the owner with an after-tax return of just 2.5 percent (not respectable) and wondering where else they can invest their capital. The “just two cents” framing Warren deploys to sell her tax is really a 62 percent confiscatory tax, and that’s under the best of circumstances.

What if the company loses money? How does the tax work then? It’s simple — the owner still owes $3 million. Without any income, they have to dip into their savings or borrow against the (declining) value of the business. To be clear, this is not a public company where shares are easy to value and sell. Borrowing for closely-held businesses is much more involved. And there are limits — what if the company is already fully leveraged?

Now take the negative effects this tax has on this one company and multiply them across the 260,000 households Warren’s bill targets. It’s easy to see the behavioral response will not be negligible but very, very robust. Just ask California, New York, Washington, the UK, Spain, Norway, and other jurisdictions experiencing rapid outmigration.

Warren’s bill will not pass this Congress, but the proposal does not have to become law to do damage. As with the California initiative, the threat alone accelerates restructuring, departures, and capital flight. In the end, the disruption to business and investment will be higher than expected, and the revenue raised will be lower than advertised. As the adage goes, you can’t draw blood from a stone.