If you follow financial news, you could be forgiven for thinking the American economy begins and ends with Nvidia, Apple, and a handful of other S&P 500 giants.

But a recent analysis from Apollo’s Torsten Slok offers a useful reminder that the companies generating all that media heat represent a much smaller slice of the actual economy than the coverage suggests. And the numbers, read carefully, point straight to Main Street.

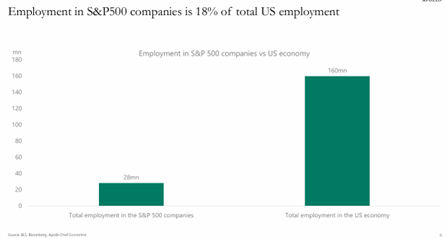

Slok’s data shows that S&P 500 companies employ roughly 18 percent of the total US workforce and account for about 21 percent of all capital investment in the economy. Privately owned firms, by contrast, drive nearly 80 percent of job openings and represent 81 percent of companies with revenues over $100 million. That’s the economy most Americans live and work in:

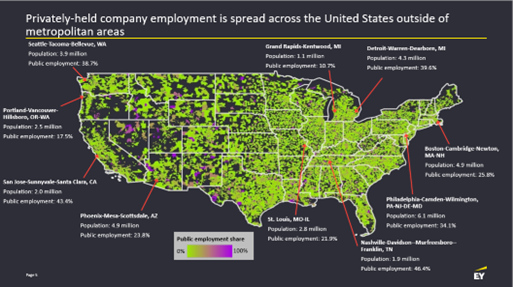

The distinction between private from public companies has geographic implications as well. Our EY study on job location includes this heatmap showing that while most public company jobs are located in city centers and the coasts, the jobs offered by Main Street enterprises are more evenly distributed across the country, forming the economic base for thousands of local communities and towns in every state.

The importance of Main Street businesses to investment and jobs is a point S-Corp has been making for years, and it goes a long way toward explaining why policies like 199A permanence and SALT Parity have been our top priorities for years. The businesses that depend on these policies are the ones doing the bulk of the hiring, investing, and growing across the American economy.

Slok entitled this report “Public Markets are a shrinking part of the US economy” but somebody forgot to tell Wall Street that. Despite the importance of Main Street to investment and jobs, roughly half of country-wide corporate profits are earned by the S&P 500. That is a remarkable concentration of earnings power, and it’s reflected in the market capitalization of US publicly traded companies relative to GDP. That ratio has nearly tripled since the financial crisis and is now well above 200 percent:

So what’s driving the disconnect between the economic dominance of Main Street and this massive capital diversion to Wall Street?

Our take is these elevated valuations are the result of a structural tilt toward public companies – they enjoy access to public equity and debt markets and they pay significantly lower effective tax rates.

As we’ve noted in the past, most public company shareholders pay little or no tax, resulting in a double benefit to those businesses. They have access to cheaper capital on the public markets, and they pay lower taxes on the returns they get from the investments that cheap capital finances.

It’s one more reason rate parity underpins our advocacy efforts.

Slok is right that public markets get more attention than their share of the economy warrants. The deeper takeaway is that the businesses most responsible for employment, investment, and economic activity in communities across the country operate largely outside the spotlight. Keeping their tax and regulatory environment competitive is how you keep that engine running.