Treasury has its hands full with the new tax overhaul. As technical comments from the US Chamber, AICPA and S-Corp make clear, the list of necessary guidance for the business community is long and growing.

Common to all three lists is the issue of aggregation. This technical sounding challenge looms large for businesses trying to calculate their pass-through deduction for 2018. For many of them, the question of whether to aggregate or not could mean the difference between getting the full 20-percent deduction or not.

To emphasize the importance of this issue, more than 40 trade groups, including the US Chamber of Commerce, the National Restaurant Association, the Farm Bureau, and the S Corporation Association, wrote to the Treasury Department today and asked for rules granting pass-through business owners the ability to aggregate (or group) multiple legal entities together when calculating the new deduction. As the letter notes:

Allowing taxpayers to aggregate or “group” legal business entities together for purposes of calculating the pass-through deduction is vital to making the deduction fair and workable. Main Street businesses often utilize multiple legal entities for non-tax business reasons. For example, family businesses are often organized in a “brother-sister” structure, where their operations are housed in one entity and their real estate in another. Another common practice is for a business to place all its payroll, finances, and insurance in a “common paymaster” entity in order to streamline payroll operations, while housing actual production operations elsewhere.

Section 199A permits owners of pass-through businesses to deduct up to 20 percent of qualified business income. Certain services businesses are precluded from this deduction, however, while even eligible businesses are subject to two alternative limitations, one based on the businesses’ payroll and another on a combination of payroll and capital.

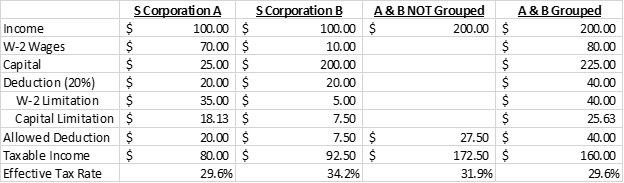

Absent aggregation, the application of these limitations would treat similar businesses differently depending on how they are organized. For example, a manufacturing business housed in a single S corporation may be eligible for the full deduction, while a similar business utilizing the common paymaster model described above may be eligible for none of it, despite having the same robust levels of payroll and investment.

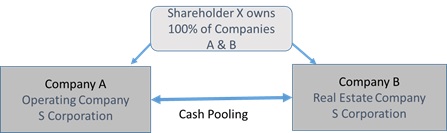

The illustration below highlights the challenge. This brother-sister set-up is a common practice operating companies use to manage their risk, costs, and ownership needs.

In this example, Company A houses the operations and employees, while Company B houses the business’ capital assets. This business is a real, operating company with robust levels of employment and investment. It should get the full deduction.

When you combine this organizational structure with the employment and investment guardrails, however, the result is a smaller deduction than if all the businesses employment and assets were housed in a single legal entity. Artificially limiting the pass-through deduction based on the unintended interaction of business structures and the new guardrails was clearly not Congress’ intent. Treasury should establish broad grouping rules to address this challenge.

It has little to lose taking this approach. Allowing businesses to aggregate or group under Section 469 would not open the door for gaming. As the business community letter states:

Allowing aggregation or grouping will not open the new deduction to gaming opportunities because the wage and investment limitations provide a strict cap on the size of the deduction, regardless of how it is measured, while the new rules could ensure that income from excluded service activities is not taken into account for purposes of the calculation.

On the other hand, blocking businesses from grouping is unlikely to save the Treasury revenues. Pass-through businesses who are in danger of not getting the full deduction have options – they can reorganize their business operations in order to access the full deduction, or they can convert to C status and get the new 21 percent tax rate. In either case, Treasury unlikely to gain any additional revenues, but the businesses themselves will be worse off. Again, the business letter makes the case:

Failure to allow aggregation will force many affected businesses to reorganize, utilizing a different combination of pass-through structures or reorganizing as C corporations. Moving business activity from one form to another, particularly a form that is going to be taxed at just 21 percent, will not save the Treasury revenues, but it will impose significant transaction costs on these businesses. They will be forced to change not just their legal organization, but also how they operate and their ownership structure. The net result will be less investment and job creation.

Now that the tax overhaul is enacted, Washington’s overriding concern should be to ensure the new law works for taxpayers and the economy. Allowing pass-through businesses to group entities together under Section 469 would prevent a massive amount of dislocation in the economy, and allow real businesses with real operations to get the full deduction Congress voted them.