WSJ is Wrong on SALT Parity

To whoever signed off on yesterday’s Wall Street Journal editorial attacking the ability of Main Street businesses to deduct their SALT payments – just like C corporations do – S-Corp has a bridge to sell you. Seriously, you got played.

The piece starts off wrong and gets worse from there. Here’s what it says:

Senate Republicans appear to be acquiescing to demands by House Republicans from high-tax states to raise the $10,000 limit on the state-and-local tax deduction to $40,000. In return for this gift to spendthrift progressive states, they should at least close a giant loophole in the cap.

The $10,000 cap on the state-and-local tax deduction was one of the 2017 GOP tax reform’s main achievements. But the dirty little secret is that many wealthy denizens of high-tax states aren’t affected since three dozen states have created a loophole for owners of and partners in pass-through business entities.

So the 36 states that have enacted our SALT Parity bills – including Alabama, Georgia, Louisianna, Oklahoma, Utah, Montana, Idaho, North Carolina, Nebraska – are all “spendthrift progressive” states? Tell Georgia Governor Brian Kemp, who signed the Georgia SALT Parity bill, to his face that he’s just the same as “Gavin Newsom and J.B. Pritzker.”

And the millions of pass-through business owners in those states – including manufacturers, retailers, home builders, and more – are just “wealthy denizens”? What a joke. A reader without any history here would think only “partners in law and accounting firms, hedge funds, consulting shops and physician practices “are able to deduct their business SALT,” but those businesses reflect a tiny minority of the pass-through community.

The comparison to wage earners is deeply flawed, too. SALT Parity critics often argue the policy is unfair to non-business owners, but they never back it up with any numbers. It’s true SALT Parity allows business owners to deduct their SALT – just like C corporations – but wage earners get benefits too, including tax-free retirement and health benefits, employer-paid FICA, and other advantages over the typical business owner.

The correct comparison for SALT Parity is with the corporate competition, who under the Senate bill continue to deduct all their SALT with no limitation and pay a really low, 21-percent tax rate. So Home Depot deducts its SALT, but not the hardware store around the block. CVS gets a full SALT deduction, but not your local pharmacy. It didn’t make sense in 2017, and it doesn’t make sense now. The WSJ is silent on this issue.

What they do care about, apparently, is the possibility of using the SALT Parity laws to game the system and generate federal tax deductions in excess of what the owners would otherwise pay and then use tax credits to make the taxpayer whole. While some states like Massachusetts are guilty of some version of this, the problem is wildly overstated and ignores simple fixes that would prevent gaming from taking place.

For example, the piece cites the Wisconsin Salt Parity law as a problem:

In Wisconsin, pass-throughs pay a flat 7.9% tax rate, which is higher than the state’s top marginal rate of 7.65%. Though individuals may pay more in state tax because of the workaround, they are still better off because they can fully deduct their SALT bills.

We wrote the Wisconsin law and the 7.9 percent rate had nothing to do with generating excess deductions – the state had an existing election where pass-throughs could pay at the entity level. We simply piggy-backed Wisconsin’s SALT Parity election on an existing Wisconsin provision, which meant the business would have to pay at the corporate rate – 7.9 percent. Question to the WSJ – why is a Wisconsin C corporation able to fully deduct their 7.9 percent tax, but if a pass-though does it, it’s a threat to democracy?

The entire editorial is in a similar vein, full of half-truths and massive distortions. We knew the Corporate Industrial Tax Complex has little sympathy for Main Street businesses and really hates our SALT Parity campaign, but seeing them manipulate the WSJ into publishing this ridiculous editorial is very disappointing.

Setting the Record Straight on 199A

Critics of the Section 199A passthrough deduction are back in full swing. A recent release by Senate Finance Committee Ranking Member Ron Wyden (D-OR) claims the House-passed proposal to extend and modestly expand the 199A deduction “disproportionately benefits the rich.”

Senate and House tax-writers need to ignore the critics and support 199A, including the House proposal to increase the deduction to 23 percent. The Wyden release may generate headlines, but it doesn’t change the underlying facts: Section 199A is one of the most effective tools to spur economic growth and job creation while helping level the playing field between Main Street businesses and large corporations.

Parity is Key

A key goal of Section 199A is to avoid placing America’s privately held businesses at a tax disadvantage relative to their C corporation competitors.

The 2017 Tax Cuts and Jobs Act (TCJA) cut the corporate rate from 35 percent to 21 percent, a historic reduction that dramatically lowered the tax burden on large (and typically publicly-traded) corporations. Meanwhile, the top rate on pass-through income was set at 37 percent and pass-through businesses generally lost their ability to deduct SALT as a business expense. C corporations continued to deduct all their SALT.

Enter Section 199A, which provided a deduction of up to 20 percent on qualified business income, thus narrowing that disparity.

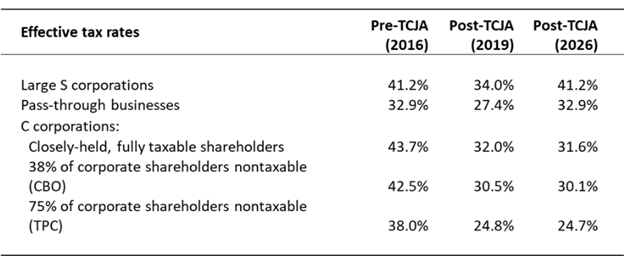

Did it completely level the playing field? No. As our EY study from 2023 showed, pass-throughs and C corporations pay similar levels of tax, but only if the pass-through deduction is available and only if lots of the C corporation’s shareholders actually pay tax. For multinationals with lots of tax-exempt or tax-advantaged shareholders, they continue to have a clear advantage when it comes to effective tax rates.

Guardrails Still Apply

Critics also gloss over the fact that Section 199A includes built-in protections that restrict the deduction for high-income owners unless they create jobs or invest significant amounts of capital.

Specifically, once a pass-through owner exceeds the income threshold of around $400,000, the deduction is limited to 50 percent of W-2 wages paid, or a similar formula applies to significant investments in property. A Treasury Department study found these guardrails exclude nearly 40 percent of pass-through income.

In other words, successful pass-throughs do get the 199A deduction, but only if they employ lots of people or make significant investments.

199A is “Neutral”

The Wyden release says most of the benefits of the 199A deduction go to high-income business owners, but a recent CRS report flatly states that the 199A deduction is neutral regarding progressivity – “The Section 199A deduction appears to have little effect on vertical equity, as it does not appear to diminish the progressivity of the federal income tax.” As the report explains:

The deduction has little effect on vertical tax equity. In theory, it reduces statutory marginal tax rates by the same factor (20%), leaving a progressive rate structure intact for pass-through business owners.

Nonetheless, available evidence indicates that high-income taxpayers might capture much of the Section 199A deduction’s overall benefit. Such an outcome would be consistent with what is known about the income distribution of pass-through business profits.

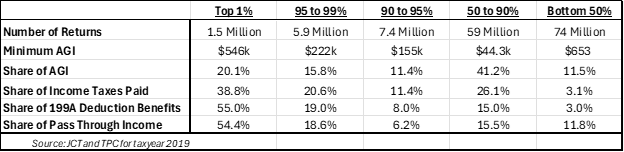

We put together this table to illustrate what the CRS report is talking about. As you can see, in 2019 the top 1 percent of taxpayers earned 54 percent of pass-through income and received a similar level of 199A deduction benefits:

Again, large pass-throughs get the 199A deduction, but only consistent with the amount of taxes they pay, and only if they employ lots of people and/or make significant investments.

Offsetting Provisions

Finally, it is important to remember that Section 199A was not enacted in a vacuum – it was part of a package that included many tax hikes. These included the caps on SALT deductions, excess loss deductions, interest deductions, repeal of the manufacturing deduction, etc.

Many of these provisions are permanent and all of them raise taxes on pass-through businesses, primarily larger ones. If the concern is progressivity, it’s clear the combined individual and pass-through provisions in the TCJA made the Tax Code more progressive, not less.

Conclusion

The Senate is moving quickly to pass its version of the Big Beautiful Bill Act, too quickly to do a deep dive on exactly who pays what under all its provisions. What is clear, however, is a robust 199A is more important than ever, particularly if the Senate keeps the 50-percent haircut on all PTET deductions. To offset these tax hikes, the Senate should adopt the House 23-percent 199A deduction and to help restore parity between Main Street and their C corporation competition.

Main Street Tax Relief Still Popular

Punchbowl News is out with a story on how the reconciliation bill before the Senate polls poorly. The DC media loves to throw shade at the BBB. Something that definitely polls well is extending the TCJA’s policies benefiting Main Street businesses.

As last month’s Winston Group poll found:

From the electorate’s perspective, government spending is by far the bigger problem than not enough revenue coming from taxes (70-21). Independent voters also see spending as the larger problem at 68-20. Inflation is still a major concern, with almost half the electorate (49%) believing that inflation is getting worse, rather than better (30%) or not changing (18%).

Given this economic outlook, voters are opposed to a tax increase in this environment: With the country still dealing with inflation, now is not the time to raise taxes (62-25 believe-do not believe). This belief is even higher among conservative Republicans (71-17) and Republicans (68-20). Independents also believe this 58-27.

So it’s no surprise that the tax provisions that support Main Street businesses remain broadly popular. Voters know these policies work and have seen firsthand the way they benefit countless communities nationwide. Efforts to extend these provisions aren’t just good policy; they’re good politics too.

Another thing voters support? Leveling the playing field between pass-throughs and C corporations when it comes to SALT:

- 82 percent agree that pass-throughs should be treated the same as corporations when it comes to deducting these taxes;

- 68 percent of voters support allowing small and family-owned businesses to deduct SALT as a business expense;

- Nearly two-thirds said eliminating the deduction would cause more businesses to fail; and

- 71 percent said Main Street businesses should be using that revenue to raise wages and provide benefits—not send it to Washington.

These are not small majorities. They reflect a clear and consistent message: Voters want tax parity, not new burdens on Main Street businesses.

The goal of reconciliation should be to make pro-growth tax policies permanent, not to punish pass-throughs with complex rules and hidden tax increases. Main Street has weathered enough challenges in recent years. This is the moment to give them the certainty they need to grow and thrive.

Avoiding Tax Hikes in the Big Beautiful Bill

The Main Street community needs the Big Beautiful Bill to succeed. Absent congressional action, taxes on pass-through businesses of all sizes will go up sharply. The same applies to most families. So the Main Street Employers Coalition supports efforts in both the House and the Senate to extend the sunsetting provisions from the Tax Cuts and Jobs Act.

Comparing the two approaches, the House bill is more friendly to small- and family-owned businesses. It increases the Section 199A pass-through deduction to 23 percent and its disallowance of Pass-Through Entity Taxes (PTETs) is limited to Specified Service Trades or Businesses (SSTB) only.

The Senate draft, on the other hand, keeps the current 20-percent 199A deduction and would apply a 50-percent haircut to all PTETs over a $40,000 threshold. Those two changes increase pass-through collections by about $140 billion relative to the House bill. Under the Senate bill, many pass-through businesses will see their taxes go up relative to what they currently pay. That was not the plan initially outlined by the President or congressional leadership.

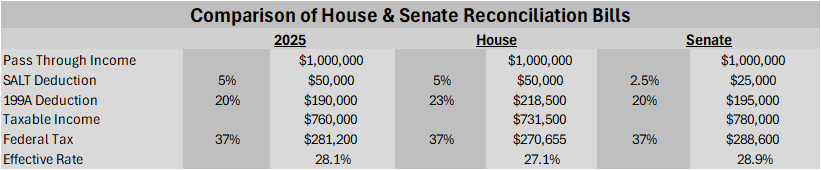

These tables show the net effect of the House and Senate policies on an example S corporation, assuming a SALT rate of 5 percentage points. As you can see, the House bill would reduce the S corporation’s effective tax rate by one percentage point, while the Senate bill would increase the rate by a similar amount.

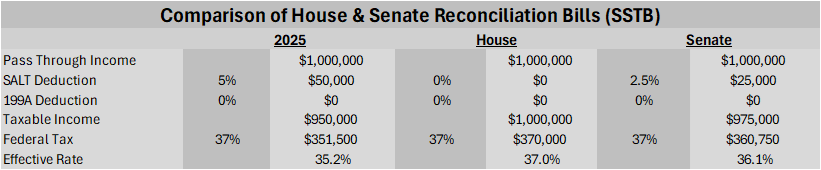

This result is not true for all pass-throughs. The House bill would have precluded so-called SSTBs from deducting their SALT. Those businesses are already excluded from the 199A deduction, so their effective tax rate under the House bill would go from high to higher. Non-SSTB businesses, however, would not be affected by the disallowance. The high marginal rates on SSTBs are the reason so many doctors and accountants are organized as C corporations.

Speaking of C corporations, both bills include increased bonus depreciation, R&E expensing, and a more friendly cap on interest deductions. While some pass-throughs may benefit from these provisions, the bulk of the benefits would accrue to public C corporations. Worse, many pass-throughs who would otherwise benefit may be blocked by the excess loss limitations included in both the House and Senate bills. These rules punish pass-through business owners for using investment income to fund job-creating businesses by disallowing them from realizing the related losses.

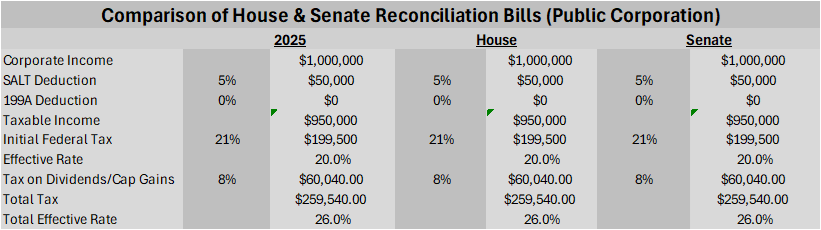

For comparison purposes, this table shows the effective rate for a public corporation under the House and Senate bills. The dividend/capital gains tax rate is 8 percent to reflect the fact that only one-quarter of public corporation shareholders are fully taxable. The remainder are made up of tax-exempts, foreign shareholders, and qualified retirement plans.

Under either bill, successful pass-through businesses would continue to pay significantly higher tax rates than their C corporation competition.

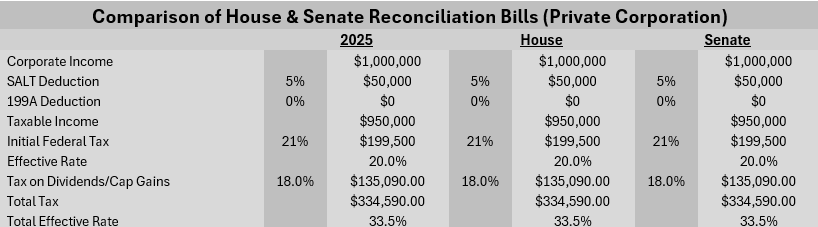

For those wondering why the S corporation doesn’t convert, this table makes clear why that’s not an option. Unlike public C corporations, the shareholders of private companies do pay taxes and those companies are under greater pressure to pay regular dividends, so the second layer of tax bites hard. We use an estimated rate of 18 percent.

These differences result in a tax rate that is 8 percentage points higher than the public C corporation. The private business pays more either way.

As noted above, these tables reflect changes to 199A and SALT policies only. They do not reflect many other changes included in the bills, changes that largely benefit C corporations but can also benefit pass-throughs. Some pass-throughs might do better than these tables suggest. They also might do worse, as both the House and Senate bills include numerous provisions that would increase taxes on pass-through businesses and their owners. These provisions include the extension and expansion of the excess loss provisions, new itemized deduction limits, and others.

The bottom line is while the Main Street community needs the Big Beautiful Bill to succeed, the House and Senate approaches are not equal. The House bill is clearly more friendly to Main Street, whereas the Senate bill focuses more on public C corporations. For both the House and the Senate, avoiding tax hikes on Main Street businesses should be a priority. As the BBB moves through the process, we will be working to ensure the legislation succeeds and that it avoids raising taxes on pass-through businesses.

Tax Notes Highlights House SALT Limitation

As we wrote recently, there’s lots to like about the House reconciliation package, but a dramatic expansion of B-SALT continues to give Main Street heartburn.

A new piece in Tax Notes lays out just how much pain the new regime would cause. Appropriately titled, “More SALTy Than Sweet?” the article beings:

Perhaps most importantly, the new SALT regime would allow for the continued viability of PTET regimes only in certain circumstances. However, PTET regimes would no longer be available in a variety of circumstances, and those circumstances are broader than an initial read might suggest.

Translation? Under the House bill, hundreds of thousands (millions?) of family-owned businesses would lose their SALT parity deductions. The article continues:

The proposed definition of qualifying entity contains many ambiguities and uncertainties and would place many administrative burdens on taxpayers… Perhaps most importantly, the qualifying entity definition does not appear to serve a clear policy purpose.

This is a core concern: the B-SALT rewrite is so complex that even top tax experts can’t figure out how it would work. The provision’s ambiguous definitions would force Main Street businesses to become tax policy sleuths just to determine if they qualify.

Is there a point to all this complexity? As the article notes:

It is unclear what pressing policy objectives are served by having both [the QTB requirement and the qualifying entity test] in the OBBB.

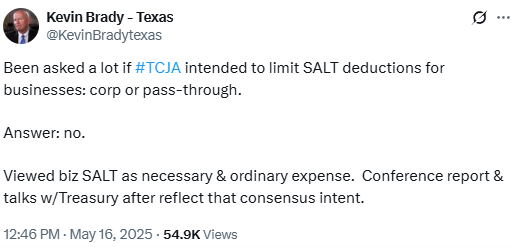

According to former Ways & Means Chairman Kevin Brady, none of this was part of the plan:

So why are we doing this? At a time when lawmakers are promising simplification and tax relief, the B-SALT expansion represents the opposite: a remarkably complex set of new rules and a massive, $80 billion tax hike on a significant part of the economy.

There’s still time for the Senate to fix this. As Tax Notes concludes:

Prompt feedback to policymakers is vital — extra cooks and taste testers may make the regime slightly less SALTy.

We agree. If lawmakers are serious about enacting pro-growth policies, they need to scrap this half-baked B-SALT expansion and focus on delivering much-needed relief for Main Street.