NIIT? Just Say Nyet

Long-time S-Corp ally George Callas is out with a great piece on the history of the NIIT and how the effort to expand the tax to active business income is nothing more than a money grab built on revisionist history. Congress exempted active business income from the NIIT on purpose, and for good reason.

This is a big deal for S corporations. As George explains:

Despite this extensive effort by both Congress and Treasury to limit the NII tax to taxpayers who “lived off investments,” the proponents of higher taxes are now characterizing the exemption of active business income as some sort of unintended loophole that should be closed. In 2021 then-President Biden first proposed this tax increase in his fiscal 2022 budget proposal, claiming that the current design “is unfair, inefficient, distorts choice of organizational form, and provides tax planning opportunities.”

Later that year, the House passed the Build Back Better Act, which adopted the Biden proposal and raised $252 billion over 10 years. The Ways and Means Committee described the proposal as closing “the loopholes that allow some wealthy taxpayers to avoid paying the 3.8 percent Medicare tax,” but — as with the creation of the NII tax in the ACA — failed to put any of that revenue into the Medicare program. Rather than extend Medicare solvency, the House preferred to use the money to pay for new social programs and green energy subsidies.

So while most C corporation income is taxed at a flat 21 percent with no additional tax owed – most C corporation shareholders are tax free or tax advantaged, after all – the focus by some policymakers is to take the higher pass-through rates and push them even higher:

Imposing the tax on business owners whose business income is subject to the top federal income tax bracket would increase their marginal rate from 37 percent to 40.8 percent. (The subset of this income that is eligible for the 20 percent deduction for qualified business income would see its marginal rate increase from 29.6 percent to 33.4 percent.)

Would these higher rates result in more revenues? Not likely.

[A] new study by three economists at the Joint Committee on Taxation estimates that the revenue-maximizing individual income tax rate is only about 40 percent, meaning that as one approaches that tax rate — say, from 37 percent to 40.8 percent — little added revenue is raised because the resulting economic damage reduces revenue in an amount roughly equal to the revenue raised by the tax directly. That the proposal’s negative impact on GDP largely offsets the direct revenue raised casts doubt on previous revenue estimates that failed to account for the proposal’s macroeconomic impact.

Meanwhile, we are all worse off:

But if the revenue effect is a wash, the economic effect is not. Revenue-maximizing does not mean economy-maximizing, and the fact that we are even approaching the revenue-maximizing rate is evidence that such high rates are damaging the economy. As Jared Walczak, senior fellow at the Tax Foundation, says, “The slope of the curve before it goes flat is highly relevant here” (emphasis in original). And as that slope’s steepness declines, Americans are made worse off.

Where does that leave us? George sums it up nicely:

Make no mistake — Biden, Harris, and others are engaging in revisionist history to justify increasing tax rates by nearly 4 percent on family businesses and risk-takers. They want to complete the deception by turning the unearned income Medicare contribution into something that is neither on unearned income, nor about Medicare, nor a contribution. The idea should be abandoned.

Exactly.

CTA Catch-22

Yesterday, the House Rules Committee declined to make in order an amendment to the National Defense Authorization Act (NDAA) that would have protected Main Street businesses from the CTA’s burdensome beneficial ownership reporting requirements. The amendment, led by Representatives Warren Davidson and Michelle Fischbach, was ultimately left out of the 312 amendments made in order for floor consideration.

Apparently, Rules was concerned that the amendment was not germane to the defense bill. That’s odd, given the CTA originally became law by riding on the NDAA back in 2020.

The decision also came despite more than 60 trades, including the S Corporation Association, strongly urging congressional leaders to include the language in this year’s NDAA. As their letter reads:

The Administration’s deregulatory agenda has removed a significant layer of uncertainty and red tape from the economy…One such regulation is the burdensome and unconstitutional beneficial ownership information (BOI) reporting mandate for 32.6 million small businesses. In March of 2025, Treasury exempted over 32 million American businesses from the reporting mandate. This action was the largest deregulatory action of 2025, saving small businesses from over $128 billion of regulatory costs and compliance burdens. This deregulatory action was monumental. However, over 32 million American small businesses fear this $128 billion regulation will come back under a future Administration. If BOI is reimposed, the significant penalties for small businesses, up to a $10,000 fine and two years in prison will be back in effect.

We are grateful for this victory, but this victory is only temporary. The fight is not over. We urgently ask that the House and Senate prioritize legislation to lock in the $128 billion of regulatory savings. This can be done through full BOI repeal, which has 34 Senate cosponsors (S. 100) and 194 House cosponsors (H.R. 425), or through language to codify Treasury’s interim final rule from March 2025 exempting U.S. businesses from BOI and destroying the BOI of the millions of American small businesses who registered with FinCEN but are no longer required to file.

The codification legislation has already passed the House Financial Services Committee. Now, it must be included in must-pass legislation like the National Defense Authorization Act (NDAA), which is how the invasive BOI mandate became law in 2021. Small businesses believe that just as Congress created the BOI mess through the NDAA, Congress can also clean up their mess through the NDAA.

This wasn’t a fringe effort. The amendment attracted nearly 40 House cosponsors, and dozens of national trades called for inclusion of the amendment.

Nor has opposition to the CTA been confined to one party. Once lawmakers fully understood the scope of the reporting mandate, bipartisan concern followed. Last Congress, the House unanimously passed legislation sponsored by Representatives Joyce Beatty (D) and Zach Nunn (R) delaying implementation of the reporting requirements by a full year. Democrats and Republicans alike recognized that requiring millions of family businesses to file ownership CTA reports under threat of criminal penalties was a far cry from the narrow anti-money laundering tool many had envisioned.

The House setback is disappointing, but it is hardly the end of the story. Attention now shifts to the Senate, where Senator John Kennedy has introduced legislation to codify Treasury’s exemption and require the deletion of previously collected BOI data, while Senator Tommy Tuberville continues to press for full repeal of the CTA. Both proposals could be considered when the Senate takes up its version of the NDAA.

The fight also continues in the courts. The National Small Business Association and the National Federation of Independent Business have each petitioned the Supreme Court to review their respective challenges to the CTA. Those petitions present the Court with an opportunity to rule that Congress exceeded its constitutional authority by compelling millions of small businesses and other legal entities to report their beneficial ownership information to the federal government.

Finally, final rules codifying the Administration’s roll-back of the CTA are pending before the Office of Management and Budget, promising that we will get final rules on the newly limited CTA in short order, hopefully coupled with the purging of existing database, as promised.

So for now, one step back and one step forward, with several tentative steps to come. It’s a strange dance, but then the CTA is a strange law. For our Senate friends, if the NDAA was an appropriate vehicle to create the Corporate Transparency Act, it ought to be an appropriate vehicle to fix it.

A Tale of Two Studies

The Brookings Institution is out with two new tax studies, one great, one not so much.

The great one is a paper by Bill Gale, Adam Looney and Elena Patel calling for a border-adjusted cash-flow tax. This is something S-Corp supported when it was debated in Congress back in 2016, and it’s still a good idea. Why? It would balance out tax rates between industries and financing methods, it would eliminate the need for all those ridiculous international rules, and it would fit nicely into a corporate integration regime that would level the playing field for close-held businesses and their publicly owned counterparts. As the Tax Foundation noted back in 2016:

Corporate integration would accomplish many of the same goals as a corporate rate cut, such as making the U.S. business climate more competitive. It could also end several economic distortions created by the current tax code, including the tax preference for debt financing over equity financing.

It would also raise beaucoup bucks that could be used to reduce taxes elsewhere. Here’s the key graph:

This package would increase investment, simplify the corporate tax, reduce distortions, and raise revenue in a progressive manner. The authors estimate that, taken as a whole, the proposal would raise over $4.7 trillion over 10 years. Even without the border adjustment, the domestic reforms alone would raise about $1.5 trillion over 10 years and make the corporate tax system simpler and more efficient, although they would not address profit shifting or international rate competition.

The border adjustment is key, as it ensures that products produced in the US are taxed in a similar manner to those produced elsewhere. It converts the corporate tax from a tax on domestic production to a tax on domestic consumption such that it doesn’t matter where a product is produced – if it’s consumed in the US, the tax treatment is the same.

So a nice addition to the tax reform discussion.

On the less good side of things, however, there’s another new paper cheerleading rate hikes on Main Street under the premise that the “U.S. tax system raises insufficient revenue to meet national needs.” Apparently, large pass-throughs are to blame.

The citation for this assertion is a Tax Law Center paper offering a general critique of the OB3. Missing is a recognition that 1) tax collections are above their fifty-year average and growing, 2) the tax code is more progressive than it’s been in the past, and 3) the amount of fraud embedded in federal spending projections is simply breathtaking.

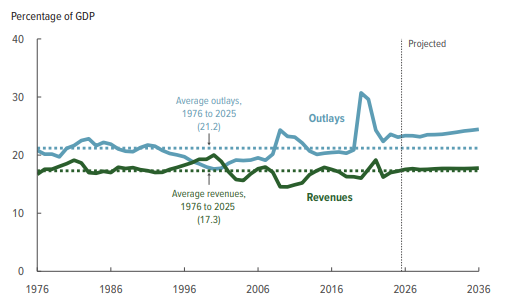

In just the last week, we’ve learned that over a quarter of Affordable Care Act enrollees are getting improper subsidies, while the GAO is out with a new report estimating improper federal payments in 2025 were $186 billion. This chart from the CBO illustrates the challenge nicely – revenues are slightly above their historic levels while spending is way higher and rising sharply.

Given all that, a mantra of “Let’s raise taxes on family businesses so we can pay for more fraud” doesn’t seem like a winning argument. Nonetheless, that’s where we are.

For S-Corp readers, the paper’s arguments will be familiar. The business tax base has eroded (it hasn’t), large S corporations pay less tax than large C corporations (they don’t), and the business community would pay more taxes if we just forced everybody back into the pre-1986 corporate tax structure (they wouldn’t).

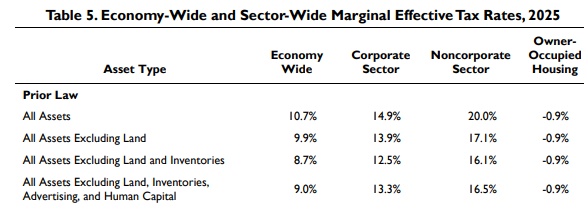

There’s too much to address in a single post (if you’re interested, we cover most of this here) but a simple reassertion of who pays what seems appropriate. Here’s the Congressional Research Service on marginal effective tax rates from last year:

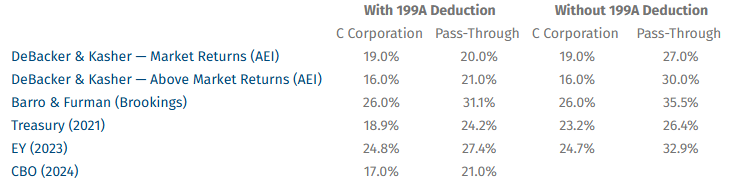

Here’s our study by EY’s Robert Carroll on how the 199A deduction affects effective tax rates:

And here’s a snappy table we put together with other sources:

What do they all have in common? They generally estimate that relative rates for pass-throughs and C corporations are similar with 199A, but pass-throughs pay more without it.

Given that most jobs are located at pass-through businesses, that’s an important observation that should instruct the direction of tax policy. The Brookings folks are correct that we face serious fiscal challenges, but casting the pass-through sector as a scapegoat based on rehashed, incorrect arguments is not going to solve the problem.

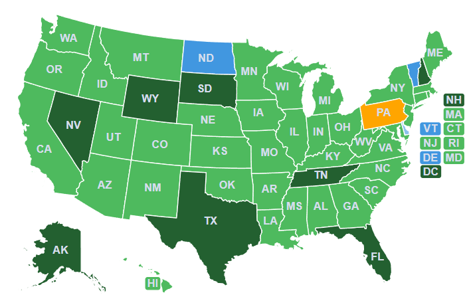

SALT Parity State of Play

Lots to report on the SALT Parity front. As you can see from our map, the number of states adopting our PTET elections is up to 38, with only four to go. It’s not all good news, however, as some states are considering backsliding on the policy while others are using the PTET regime to offset significant new taxes. Here’s the rundown.

Back in March we flagged an emerging threat to New York’s Parity regime, noting that their budget proposals included PTET “haircuts” that would siphon money away from New York’s Main Street businesses and into state and city government coffers.

The proposal included cutting the state PTET credit to 90 cents on the dollar, while Mayor Mamdani went further, requesting the state reduce the city credit to 75 cents. Fortunately, Governor Hochul opposed the proposal and, more recently, announced both haircuts were left on the cutting room floor. The existing PTET regimes in New York State and New York City remain intact.

So a good result, but not exactly a clean bill of health. The episode revealed the dark underbelly of SALT Parity — when states face a budget crunch, they often view our PTET credits as an opaque means of raising revenue.

Maine is a good example. The state enacted our SALT Parity reform just this spring, but the new PTET includes a 10 percent haircut diverting funds away from businesses and into the state’s coffers. Also included was a 2 percent income surtax on individuals above $1 million, a so-called “millionaire tax.” Taxpayers subject to the new tax will pay an extra $20,000 in state taxes for every million they earn, while splitting the new PTET credit $6,660/$740 with the state. Not a great outcome for Main Street. That’s a net tax hike for taxpayers subject to the surtax, and a smaller than expected tax benefit for those below it.

Washington State, meanwhile, is on its own journey. The state recently enacted its first-ever personal income tax — a 9.9 percent tax (seventh highest in the country) on income exceeding $1 million. The state had historically rejected imposing an income tax, with voters adopting an initiative prohibiting one as recently as 2024. That initiative means the new tax faces an inevitable legal challenge, but the Washington State Supreme Court is highly flexible and likely to embrace the new tax anyway. Bottom line, as with Maine, the enactment of the new PTET regime in Washington is a one step forward, two steps back proposition.

On the brighter side, several states have moved to extend and/or improve their PTET regimes. California extended its SALT Parity program through 2030 as part of last year’s budget and added flexibilities around election timing and payments to reduce administrative burdens. Elsewhere, Minnesota and Oregon passed extensions of their programs through 2027, while Illinois took the strongest step by making its PTET law permanent late last year. It’s a welcome contrast to the erosion we’re seeing elsewhere, and a reminder that SALT Parity shouldn’t be treated like a piggy bank.

Finally, we will ask again — what are North Dakota, Pennsylvania, Delaware and Vermont waiting for? As we’ve said from the beginning, SALT Parity is a rare win-win for states. It costs the States nothing, while their Main Street businesses get a restored business deduction. For lawmakers in those states, they are leaving billions in tax savings on the table.

SALT Parity is one of the more tangible policy wins Main Street has achieved in recent years, and we oppose efforts to quietly erode it through haircuts or other backdoor tax hikes. We’ll keep tracking (and fighting) these threats even as we vigorously wave the SALT Parity flag.

A Double Tax Trap

When tax writers approach the next round of tax reform, number one on their list should be to eliminate double taxation. Nothing contributes more to economic distortions than taxing the same income two (or more) times. Embracing a “single tax system,” on the other hand, would eliminate those distortions and encourage more investment and job creation.

The brouhaha over the new Section 68 haircut on itemized deductions suggests we’ve got a long way to go on that front. Here’s how CNBC describes the problem:

The deduction cap is imposed on trusts and estates, the experts said, which was unexpected. Even if a trust gave all its income to its beneficiaries, it would have to pay taxes on a portion of that income, according to their interpretation of the document.

While the consequences are steeper for trusts and estates of the ultra-wealthy, trusts with as little as $16,000 in income would also be subject to additional taxes, the experts said.

“There is potentially an element of double taxation,” said Dan Griffith, director of wealth strategy at Huntington Bank. “This is something that is going to affect somebody with a $400,000 special-needs trust. It’s not just going to be something that $100 million dynasty trusts suffer with.”

Griffith said he is especially concerned about trusts that are obligated to distribute all their income. Trusts will either have to sell assets to pay the taxes, sacrificing future investment returns, or reduce their distributions to beneficiaries, he said.

The Joint Committee on Taxation’s (JCT) Blue Book raised the profile of this issue by suggesting that the double tax outlined above was both the correct interpretation of the new statute and reflective of congressional intent. But is it, and was it? No, not.

What’s Affected

Contrary to the Blue Book, how the Section 68 haircut applies to deductions unique to trusts and estates is entirely unclear. As noted in a Tax Notes article Monday:

Does section 68 apply to special fiduciary deductions that only apply to trusts and estates — not individuals? Many fiduciary deductions, including those under sections 67(e), 642(b), 642(c), 651, and 661, function as mechanisms for allocating income to beneficiaries or charities. Applying section 68 could undermine subchapter J’s quasi-conduit principles and risk double taxation at the fiduciary and beneficiary levels.

Why is this important? The CNBC story above includes a nice illustration. So does the Tax Notes article:

Assume the DEF Trust received ordinary interest income of $1 million, had no expenses, and distributed $1 million to a beneficiary. The DEF Trust should have a distribution deduction of $1 million under sections 651 or 661. However, if the 2/37ths limitation under section 68 applies to fiduciary distribution deductions, then the DEF Trust will be subject to tax on $53,189.19 [($1 million – $16,000) * 2/37 = $53,189.19]. The beneficiary would still be subject to tax on the entire $1 million distribution of ordinary income, and that beneficiary’s itemized deductions would also be limited by 2/37ths under section 68. In effect, the application of section 68 to fiduciary distribution deductions would create a double tax of the same income to both the trust and the beneficiary, which would contradict the legislative intent for taxing trusts and estates under subchapter J.

Applying new Section 68 to all allowable trust and estate deductions results in a 2-percentage point increase in their effective tax rate, starting with income as low as $16,000. That is because all the trust’s taxable distributions to beneficiaries would be subject to tax, while 5.4% of the same income would be subject to tax at the trust or estate level. Income from active S corporations is at risk here, too. Consider how this would function with an estate (or a 645 trust) holding S corporation shares. This result could diminish the value of the 199A deduction by more than a quarter.

Clear Statutes, Opaque Intent

The key phrase in the Tax Notes citation above, however, is if the limitation applies to fiduciary distribution deductions. The Blue Book issued last month concluded that section 68 applies to estates and trusts in footnote 102 on page 26. But the Blue Book is not the definitive authority, nor is it legislative history — rather it is post-enactment secondary authority. Regarding the legislative history, the Tax Notes piece says this:

Neither the statutory text nor the legislative history directly addresses the application of the new limitation to preferential-rate income or to deductions unique to trusts and estates. The current statutory framework risks unintended results — such as double taxation and erosion of long-standing quasi-conduit principles — and requires targeted legislative or regulatory clarification.

Our S-Corp advisors agree. New Section 68(a) says “In the case of an individual, the amount of itemized deductions otherwise allowable for the taxable year (determined without regard to this section) shall be reduced….” The first sentence of section 642(b) however, says “The taxable income of an estate or trust shall be computed in the same manner as in the case of an individual, except as otherwise provided in this part.” [Italics added.]

The italicized language in these two statutes is key, as the disputed deductions are unique to trusts and estates, and are provided in Part I of Subchapter J of the Internal Revenue Code (“Estates, trusts, and beneficiaries”). They clearly fit within the “except as otherwise provided in this part” language. Furthermore, S-Corp is not aware of any contemporaneous expression of intent – that is, actual legislative history — that suggests legislators intended to tax more than 100 percent of trust or estate income in any circumstances.

Treasury Should Act

The combination of clear statutory text and opaque intent should be sufficient for Treasury to craft language that limits the scope of Section 68 to itemized deductions that are available to individuals only and exclude deductions that are merely income allocation provisions applicable to estates and trusts.

As the language of Reg. §1.67-4(a)(1) states: “An estate or trust…must compute its adjusted gross income in the same manner as an individual, except that the following deductions…are allowed in arriving at adjusted gross income:…(B) Deductions allowable under…sections 651 and 661 (relating to distributions)”. This is especially important as the function of sections 651 and 661 is simply to allocate income between the estate or trust and its beneficiaries, rather than to give a tax benefit, such as for a charitable contribution.

The Tax Notes author agrees. His options to clarify the provision and avoid double taxation include:

- “Congress could amend section 68to clarify that it applies only to deductions computed “in the same manner as in the case of an individual.” This would exclude fiduciary-specific deductions under sections 67(e), 642(b), 642(c), 651, and 661, preserving the quasi-conduit structure of trusts and estates.”

- “[I]f section 68is intended to apply to charitable deductions under section 642(c) but not to the unique administrative expenses of trusts and estates or to the deductions allowed under sections 642(b), 651, and 661, Treasury could issue regulations under section 68 — similar to reg. section 1.67-4(a)(1)(ii) — clarifying that those deductions are not itemized deductions within the meaning of section 63(d).”

This position and recommendations are consistent with comments from the AICPA, the NYSBA Tax Section, and ACTEC.

You can add S-Corp to that list. The JCT’s position on new Section 68 is unsupported by the statute, the tax history of trusts and estates, and the understanding of those who voted on last year’s tax bill. It is also contrary to all other secondary authorities. The bottom line is Congress and the Treasury should be spending their time eliminating harmful double taxation, not stumbling their way into new instances of it.