More Pushback on Rate Hikes

The Main Street Employers coalition organized a letter calling on tax-writers to reject rate hikes last week. More than 90 trades, including all our Main Street friends, signed on.

That effort caught the attention of Americans for Tax Reform’s Grover Norquist, who flagged it in a recent media appearance.

President Trump is not going to allow the top rate for income taxes to be increased. That is a direct hit on small businesses. There was a letter that went to the Hill from 90 trade associations that represent small businesses pointing out that subchapter S corporations that pay the individual rate would be badly hit.

…National roofing contractors, the Precision Metalformers, the Association of Builders and Contractors, heating, air conditioning and refrigeration. These are the people who make America work.

You’ve got some [people] in the White House pushing the idea that President Trump is going to break his word and raise taxes. Trump has said, again and again on the campaign, that he wanted a tax cut for everybody.

As we’ve covered previously (see here, here, here, and here), the idea is to bump top marginal rates to roughly double what public C corporations pay. What’s being dubbed as a “millionaire’s tax” would instead hit Main Street employers, raising their rates to the highest level in nearly four decades.

The buzz seems to be driven by comments from tax-writers that “everything is on the table.” That innocuous starting point has morphed into a self-perpetuating media cycle, where any response short of an outright rejection becomes headline news.

Nonetheless, the business community needs to be public in its opposition to this bad idea. Fortunately, Key Republicans feel the same way and have voiced their concerns. Here are a few responses compiled by National Review:

- House Speaker Mike Johnson (R., La.): “Generally we’re trying to reduce taxes here.”

- House Majority Leader Steve Scalise (R., La.): “No. 1 goal is keeping rates where they are and preventing a tax increase.”

- House Ways and Means Committee Chairman Jason Smith (R., Mo.): “We are going to create a tax code that grows the economy, that grows wages, is the focus to help deliver tax relief for America. The way you provide tax relief is, you cut tax rates.”

And just earlier today Republican Senator Dave McCormick of Pennsylvania:

I don’t think that’s likely to happen…We’ve got to reel in the spending. That’s going to require some tough choices. But we can’t do that by raising taxes, which slows the economy and hurts working families.

Finally, here’s economist Arthur Laffer a day earlier speaking on Kudlow’s show:

That we are even talking about a tax rate increase on the top income earners is silly. Can you imagine that conversation appearing a month ago? It makes no sense whatsoever. Trump doesn’t want to raise the highest tax rates.

This broad and swift pushback is exactly what tax-writers need to hear as they begin to craft the tax package. So take recent media reports of looming rate hikes with a grain of salt, but don’t be complacent. Make sure to let your elected officials know how you feel about raising rates on Main Street. We’ll be doing the same.

199A Deficit Account Relief

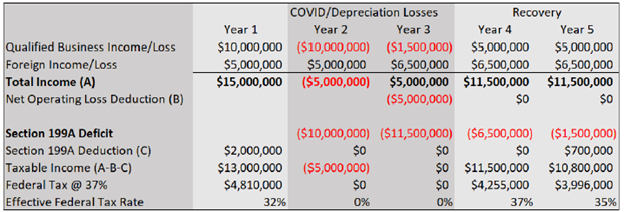

The House last week signed off on a Senate-approved budget resolution that uses a “current policy baseline” method of tallying up the bill’s deficit impact. One quirk of this approach is any existing policies must not be simply renewed but would need to include a substantive change from current law. That means lawmakers using a current policy baseline will need to make tweaks to the Section 199A deduction to stay compliant.

Section 199A(c)(2) bars a pass-through business from claiming the 199A deduction until it recoups 199A qualified losses from prior years—so-called “199A Deficits.” That provision has proven to be deeply unfair to many family businesses, particularly those that incurred losses during the pandemic to keep their workers employed and their doors open.

Today, many of those businesses are turning a profit again but they’re blocked from the 199A deduction because of these losses. Add to that the exclusion of foreign income and certain capital gains from Qualified Business Income (QBI) and many Main Street employers find themselves in a double bind: significantly higher taxes and no 199A deduction.

The table above helps illustrate this dynamic. The hypothetical business is being penalized for incurring losses during a time when much of Main Street was forced to cease its operations. Worse yet, this adverse outcome is not a one-time event as those deficits carry over and increase the company’s tax burden for years to come.

C corporations, by contrast, face no such hurdles. NOLs incurred by C corporations apply to all forms of income, so a C corporation with NOLs doesn’t pay tax. They enjoy a flat 21 percent rate, unlimited in scope and free from these types of constraints — regardless of whether the income is foreign or domestic.

For these reasons, Main Street supports a two-step fix that’s practical and Byrd Rule compliant. Step one is a one-time election to allow businesses to zero out their 199A deficit balances, thus giving them immediate access to the 199A deduction as Congress intended. Step two is allowing foreign-sourced income to be included in QBI. There’s simply no valid reason to exclude this income from 199A.

Adopting these two steps would make Section 199A more accessible, more effective, and more aligned with the policy’s original intent. Most importantly, they would help millions of family businesses recover, reinvest, and grow faster.

Putting the Tax Hike Debate to Rest

The House yesterday cleared a major hurdle in the effort to move a broad tax package when lawmakers signed off on a Senate-passed budget resolution. With the broad parameters of that legislation in place, Main Street is speaking out against an ill-conceived tax hike proposal. A letter signed by more than 90 trade associations reads:

The so-called “millionaire tax” in question – which actually kicks in at income around $620,000 – would saddle them with a tax hike that offsets about half the tax benefit of extending the Section 199A deduction. Coupled with the Net Investment Income Tax and state and local taxes, the proposal would impose marginal rates exceeding 40 percent on businesses that receive the full Section 199A deduction, or twice the rate paid by C corporations.

Certain industries are precluded from Section 199A, however, as is foreign-sourced income and Section 1231 gains. So-called “guardrails” tied to wages, capital investment, and taxable income reduce the value of the deduction for many more. Businesses ineligible for the full 199A deduction would face combined marginal rates above 50 percent. Rates that high are simply not sustainable.

We understand the fiscal pressures involved in crafting a legislative package of reforms and extensions, but increasing the top individual rates would target the very businesses Congress seeks to help. Proposals like this reflect a fundamental misunderstanding of how these companies operate and their central role in the broader economy.

The idea of a 40-percent top rate was floated last week and would raise tax rates on Main Street businesses to their highest level in nearly four decades. The proposal was immediately met with skepticism by Republican leaders and the opposition of the Main Street business community should make clear that raising taxes on America’s job creators is a bad idea.

As lawmakers work toward a final tax agreement, they should focus on policies that promote investment and ensure the tax code works for the real economy. Anything less is a step backward.

Getting Back to Tax Policy

With this morning’s passage of the budget resolution in the House, it’s full steam ahead on the tax policy front. Fortunately, our friends on the small business committees are focused on what’s important – Congress needs to act now to prevent a massive tax hike on millions of Main Street businesses.

That focus was on full display during a House and Senate joint hearing entitled, “Keeping Taxes Low for Small Businesses” which featured two witnesses from our Main Street Employers Coalition.

Here’s Tom Click – president and cofounder of Patriot Industries, a Virginia-based manufacturer – with more on that dynamic:

One of the most impactful provisions was the 20% deduction for small businesses, which gave pass-through entities like ours the ability to compete on a level playing field with larger corporations. This crucial tax relief enabled us to grow at a faster pace and reinvest in our company and employees. The Section 199A deduction is a critical component of the TCJA that ensures Main Street businesses can remain competitive in an increasingly challenging environment.

…For companies like ours, which employ workers, invest in communities, and contribute to local economies, this deduction has been instrumental in supporting job creation, capital investment, and overall business growth. If Section 199A is allowed to expire, the consequences will be severe for countless small and family-owned businesses across the country like ours. Many firms in our industry already operate on thin margins, and the sudden tax increase resulting from the loss of this deduction would mean a 20 percent tax increase at a time of great uncertainty in the economy. Worse yet, this tax hike would be borne exclusively by pass-through business – which currently supply more than 6 out of every 10 jobs nationwide – and would create a ripple effect across the American economy as a whole.

How would things play out if Congress failed to act? Here’s Tom again with a bleak analysis:

Finally, the expiration of Section 199A would no doubt force many businesses to be sold to larger corporations, thus accelerating the ongoing consolidation of economic power and shifting control away from Main Street and further into the hands of a few dominant corporations. These sales would be triggered not by market inefficiencies or poor business practices, but simply due to an uneven tax code that disproportionately benefits Wall Street over Main Street. This would weaken local economies, reduce competition, and ultimately harm American workers by limiting job opportunities and wage growth.

Later the panel heard from Jerry Akers, a serial entrepreneur and current owner of multiple franchise operations:

Much like the rest of small business owners, the 199A deduction has enabled me to increase investment in new equipment, technology, and facilities, driving growth and innovation, while the extra financial breathing room has allowed me to hire more employees, and provide better benefits to existing team members.

More importantly, this deduction has helped level the playing field, allowing businesses like mine to compete with larger corporations, and provide a level of financial stability that has been very valuable. The thought of these hard-earned gains being jeopardized is deeply unsettling. It’s not just about numbers; it’s about the livelihoods of families, the vitality of communities, and the spirit of entrepreneurship.

As Tom, Jerry, and the other witnesses made clear, Section 199A is not a “loophole” or “giveaway” – rather, it’s a key component of a tax system that recognizes the unique structure and contributions of pass-through businesses. These firms don’t have access to the capital markets like their publicly-traded counterparts. They must rely on their own profits to reinvest, grow, and hire.

As Congress deliberates on the current tax package, we are encouraged that lawmakers continue to focus on Section 199A and its importance to the economy. We look forward to more opportunities to showcase these Main Street success stories and get the message across.

Tax Hike Nonsense

The battle over the Budget Resolution is a spending fight, not a tax fight. There is broad agreement over how to extend the expiring individual and pass-through tax policies, whereas there are significant differences when it comes to spending reductions. The problem for Main Street is some members apparently don’t know the difference.

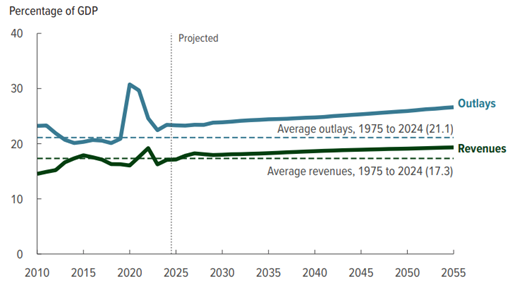

This chart from CBO tells the whole story. Revenues into the federal government are well above historic norms and rising. Spending, meanwhile, is simply out of control. The federal government used to spend one out of every five dollars as recently as 2019 – it is now one out of four and rising.

One would think any rational policymaker would take a look and conclude that they need to focus on spending, not taxes. One would be wrong. A recent Bloomberg article quotes at least two Republicans open to raising the top individual (and pass-through) rate to 40 percent. According to the piece:

House Freedom Caucus Chairman Andy Harris says he is open to the creation of a new 40% tax bracket for those earning $1 million or more, lending credence to an idea Republicans are considering as a way to offset some new tax cuts.

Harris said in an interview on Monday that he views the millionaires’ tax rate as a “reasonable way to pay for” President Donald Trump’s campaign pledge to eliminate levies on tipped wages.

“You are only raising it a couple of points,” the Maryland Republican added. The current top tax rate is 37% for individuals earning more than $626,350 a year.

The Representative is wrong that it’s a small increase – a top rate of 40 percent would be the highest level since Reagan cut rates back in 1986 – almost 40 years! It would also eliminate about half the benefit of the 199A deduction for affected businesses, assuming they actually get the deduction. For those that don’t, it’s just a tax hike.

The good news is these suggestions were quickly shot down by House leadership, who clearly have no interest in making rate hikes part of their effort to extend the TCJA provisions.

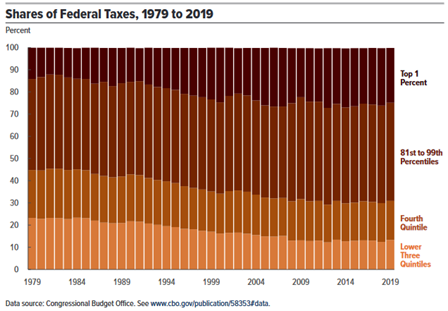

Nonetheless, the Main Street community needs to respond to these suggestions. Taxpayers paying the top rate – including about a million pass-through business owners – represent just 1 percent of all income earners but pay a remarkable 25 percent of all federal taxes.

Moreover, their share of total tax payments is large and rising, even as the top rate has come down. In 1979, the top marginal rate was 50 percent and the top one percent paid 14 percent of all taxes. Today, the top rate is 37 percent and the top one percent pay 25 percent.

Any suggestion these taxpayers are “under-taxed” is laughable.

So is the idea that our Tax Code is anything but progressive. Notice how all the dark areas in the graph reflecting higher income taxpayers is growing, while the lighter areas reflecting lower-income taxpayers has shrunk? That’s a representation of how our Tax Code has gotten more progressive over time.

We expect Congress to work out their differences on spending. We also expect them to reject calls to raise marginal rates. But the Main Street Community needs to beware. The premise that Republicans are unified in opposing rate increases is no longer valid, and we need to work to restore it.